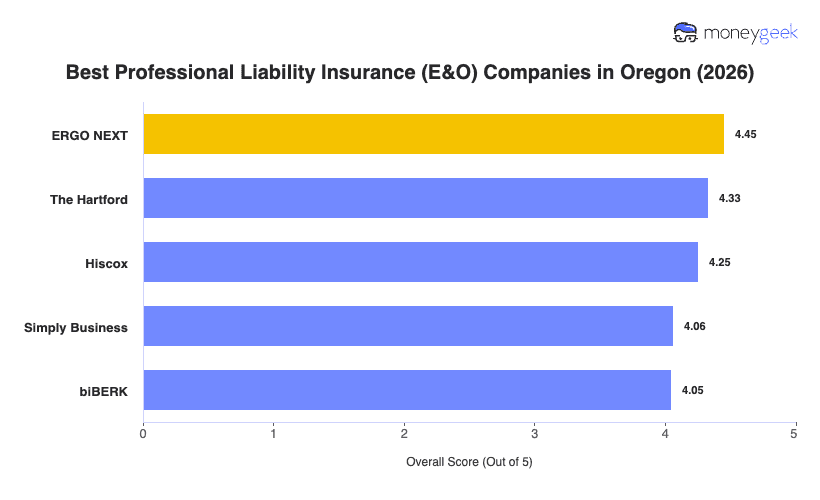

Our analysis of Oregon professional liability insurers found three providers that consistently outperformed the field across affordability, customer experience and coverage quality.

- ERGO NEXT: Rates and a fully digital buying experience that takes about 10 minutes from start to certificate of insurance put ERGO NEXT at the top of the Oregon rankings. The insurer ranks first across 14 of 18 industries in Oregon, with its strongest scores in healthcare, fitness, pet care, childcare and arts and media. Consulting, education and financial services businesses will find better rates and coverage fit elsewhere, as ERGO NEXT's pricing in those industries runs above the Oregon average.

- The Hartford: A 200-year track record and fast claims processing set The Hartford apart from most competitors in the Oregon market, particularly for consulting and financial services professionals where it ranks first in the state. The insurer lets businesses start with a core policy and layer on additional coverage as they grow, which suits Oregon's large population of small professional firms in Portland and Eugene.

- Hiscox: Tailored policies across more than 180 industries give Hiscox unusually broad reach for a small business insurer, and it ranks first in Oregon for education providers and nonprofits. The insurer's online buying process is available around the clock and its policies can cover up to five office locations under a single plan, which works well for Oregon businesses operating across multiple markets.

Ranked providers represent the best fit for most Oregon businesses, but no single list captures every consideration. Comparing business insurance options side-by-side and getting direct quotes gives you the clearest picture before you commit.