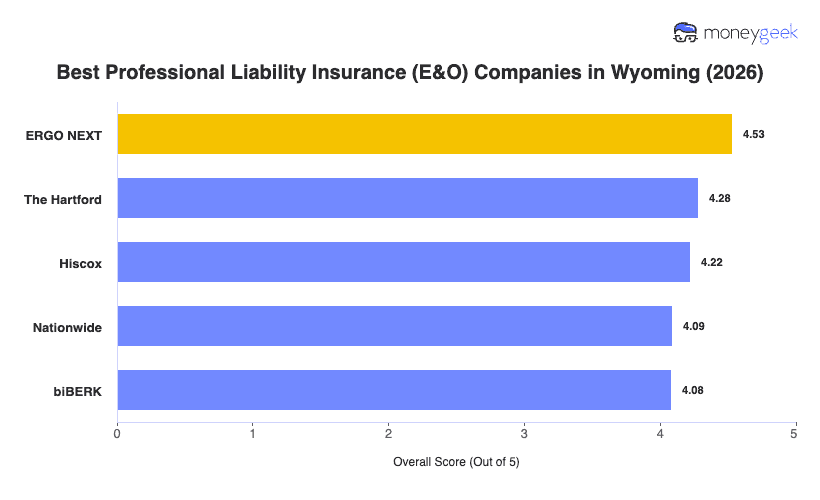

Our analysis of Wyoming professional liability insurers found three providers that consistently outperformed the field on rates, customer experience and coverage quality.

- ERGO NEXT: Topping the list on both affordability and customer experience, this digital-first insurer ranks first in 15 of 18 industries for Wyoming businesses. The buying process is fast and straightforward, with quotes and coverage binding available in minutes, which matters when a client contract hits your desk and you need proof of insurance that same day. ERGO NEXT works especially well for construction and contracting, cleaning services, healthcare, fitness, pet care, real estate and tech businesses in Wyoming. No Wyoming industry ranks it below third.

- The Hartford: A+ rated and active across multiple professional categories, The Hartford earns its spot on the strength of its industry-specific coverage options and claims support infrastructure. It ranks first or second in Wyoming for consulting services, financial services, education, hospitality and marketing, making it a strong fit for Wyoming businesses in those fields. It scores lower for healthcare providers and other professional services, where its affordability rating drops, so medical and specialty professionals should compare it carefully against other options.

- Hiscox: Built for small firms and solo practitioners, Hiscox brings a clean buying experience and strong coverage across most industries. It ranks first in Wyoming for hospitality, travel and tourism, and scores well for tech, nonprofits, childcare, beauty and wellness, and pet care. That profile fits Wyoming's business environment well, where independent operators and small professional firms make up the majority of the market.

Ranked providers represent the best fit for most Wyoming businesses, but no list captures every situation. Comparing business insurance options side-by-side and getting quotes directly from multiple carriers gives you the clearest picture of what you'll actually pay.