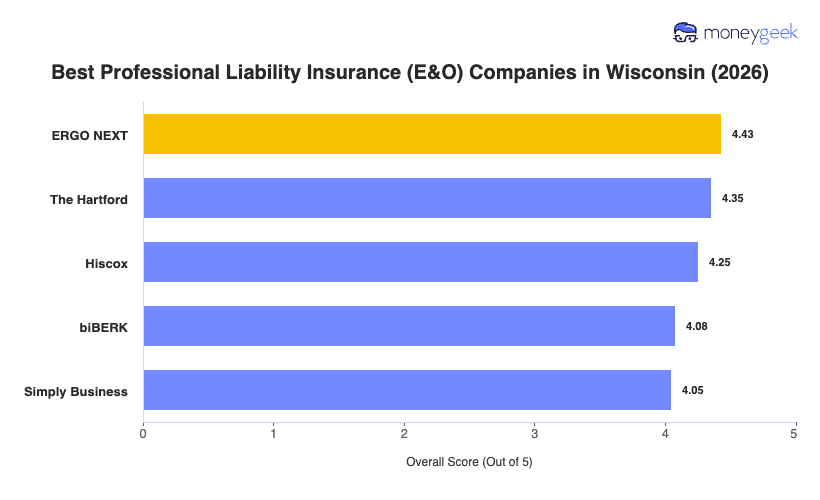

Our analysis of Wisconsin professional liability insurers identified three providers that consistently ranked above the field.

- ERGO NEXT: It ranks first across more Wisconsin industries than any other provider in this analysis, including construction and contracting, healthcare, cleaning services, fitness, pet care, real estate, marketing and other professional services. Buying a policy runs entirely online, with a certificate of insurance available immediately after purchase and 24/7 policy management through a mobile app. Consultants and financial services firms are the exception; ERGO NEXT places sixth in both categories for Wisconsin.

- The Hartford: The strongest option in Wisconsin for financial services and consulting, ranking first in both. It also takes first for education and second for marketing and tech. Professional liability claims go to dedicated specialist teams rather than a general service line. Healthcare businesses are not a good fit; The Hartford ranks ninth in that industry for Wisconsin.

- Hiscox: Ranks first in Wisconsin for both tech/IT and nonprofits, and places in the top three for consulting, financial services, childcare and real estate. It specializes in small businesses and solo practitioners, with online quotes and same-day coverage for most professions. Construction is the weak spot; Hiscox ranks seventh for that industry in Wisconsin.

These three providers are the best fit for most Wisconsin businesses, but no ranked list accounts for every need. Comparing business insurance options side-by-side before committing gives you the clearest picture.