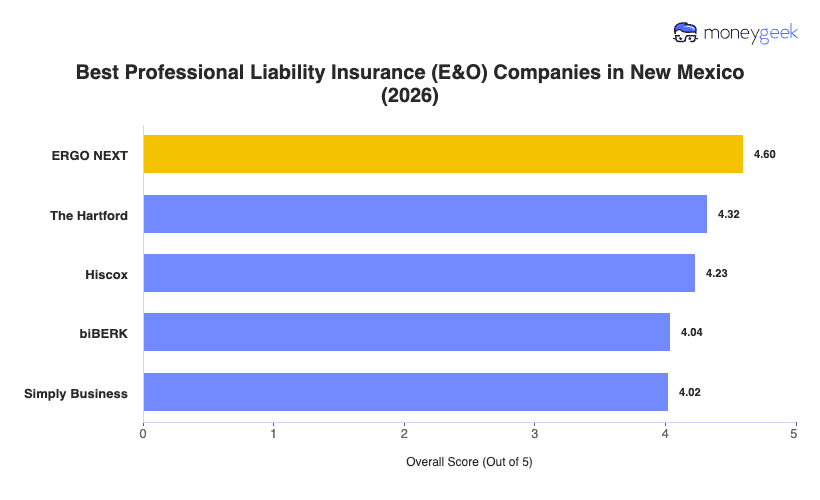

Our analysis of New Mexico professional liability insurers found three providers that consistently outperformed on rates, coverage quality and overall service experience.

- ERGO NEXT: Buying a policy takes about 10 minutes online, no agent required, with an instant certificate of insurance you can share with clients from your phone. That speed and simplicity earned ERGO NEXT the top position, and it backs it up with the lowest rates among New Mexico's top-ranked providers. The insurer ranks first overall across 15 of 18 industries in the state, making it a strong fit for the widest range of New Mexico businesses.

- The Hartford: More than 200 years in the industry gives The Hartford a depth of claims-handling infrastructure that newer digital carriers haven't built yet. It ranks first in New Mexico for Hospitality, Travel and Tourism, Real Estate and Beauty and Wellness, and its professional liability policies can be bundled directly into a business owner's policy, which simplifies coverage management for businesses that need more than one line. New Mexico businesses in healthcare or other professional services should look elsewhere, as The Hartford ranks ninth in both categories for the state.

- Hiscox: Coverage tailored to more than 180 specific industries makes Hiscox the strongest pick for white-collar professionals who need a policy that actually reflects what they do. It ranks first in New Mexico for Tech/IT and is a consistent top-two finisher for financial services, nonprofits and consulting. Construction and recreation businesses will find better-matched options with other providers.

These three providers are the best fit for most New Mexico businesses, but no ranked list covers every situation. Comparing business insurance options side-by-side and pulling quotes directly from carriers gives you the clearest picture of what's right for your business.