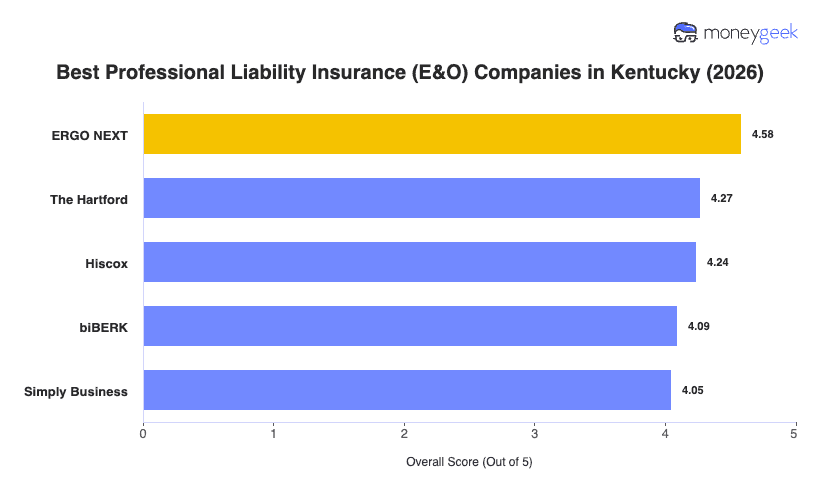

Our analysis of Kentucky professional liability insurers found three providers that consistently outperformed the field on rates, service quality and coverage breadth.

- ERGO NEXT: Affordability is the main story here, with the highest affordability score of the three and a top overall ranking driven by strong scores across every category. It ranks #1 across 14 of 18 industries in Kentucky, including healthcare, financial services, consulting, construction and cleaning services. No industries in Kentucky ranked it at the bottom of the field, making it the most broadly safe choice for most businesses in the state.

- The Hartford: Deep profession-specific coverage options earned The Hartford the second spot. It ranks #2 for arts, education, fitness, hospitality, marketing and real estate professionals in Kentucky, which reflects its strength in service-oriented businesses where client contract requirements tend to be more demanding. Healthcare and other professional services are the weak spots, where it ranks 9th, so medical practices and similar businesses should look elsewhere.

- Hiscox: Tech businesses in Kentucky get their best overall option in Hiscox, which ranks #1 in Tech/IT statewide. It also ranks #2 for consulting, financial services, beauty and wellness, childcare and nonprofits. The coverage score is competitive and it carries no industries where it ranks in the bottom tier for Kentucky.

These three represent the best fit for most Kentucky businesses, but no ranked list covers every situation. Comparing business insurance options side by side gives you the clearest picture of what each provider actually offers for your profession.