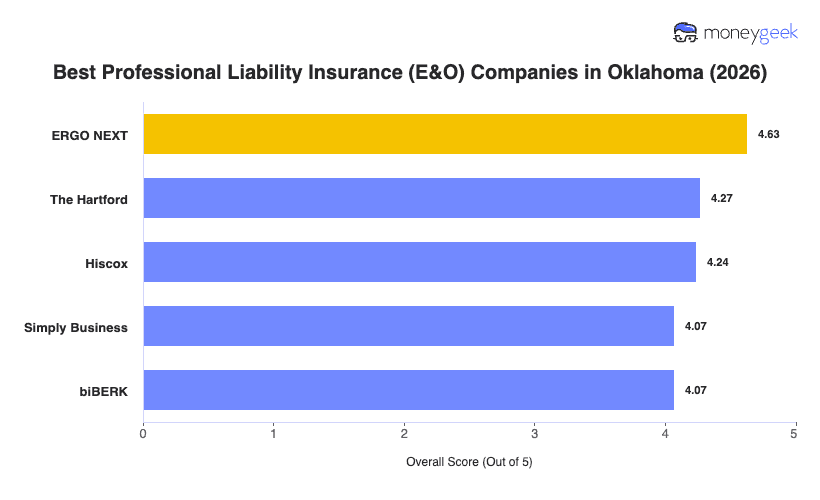

Our analysis of Oklahoma professional liability insurers identified three providers that consistently outperformed the field on rates, coverage and the buying experience.

- ERGO NEXT: Tops the Oklahoma rankings across 16 of 18 industries, with the strongest performance in cleaning services, consulting, financial services, healthcare, tech and pet care. The fully digital buying experience is a real differentiator for Oklahoma's large population of small and solo-operated businesses: you get a quote, buy coverage and pull a certificate of insurance in under 10 minutes, all without picking up the phone. One caveat worth noting for Oklahoma businesses in hospitality, food service or construction-related operations: ERGO NEXT excludes professional negligence coverage for those industries, so check your specific work type before committing.

- The Hartford: Earns its second-place position on the back of broad industry coverage and a particularly strong showing for hospitality and tourism businesses, marketing and communications firms and education professionals in Oklahoma. With more than 200 years in the business, it brings dedicated specialist support and coverage options that go deeper than most digital-first carriers, including industry-specific endorsements and access to licensed agents who know their way around professional liability policies. Oklahoma healthcare professionals and those in other professional services categories will find The Hartford underperforms relative to its overall rank in those two specific industries, so weigh that against your own needs.

- Hiscox: Covers more than 180 professions and brings genuine depth to industries like consulting, financial services, tech and childcare, all of which rank second in Oklahoma under Hiscox's coverage. It's a strong fit for Oklahoma City and Tulsa professionals in knowledge-based fields who want industry-tailored policy language rather than a one-size approach. Construction and recreation businesses rank lower with Hiscox in Oklahoma, so those professionals should compare options carefully.

Ranked providers represent the best fit for most Oklahoma businesses, but no list captures every factor your specific situation calls for. Comparing business insurance options side-by-side and getting quotes directly gives you the clearest picture of what you'll actually pay and what you'll actually be covered for.