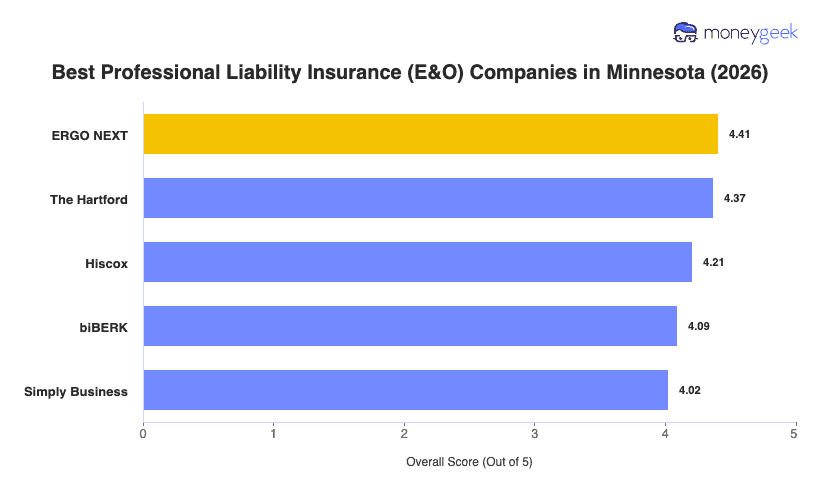

Our analysis of Minnesota professional liability insurers found three providers that consistently outscored the field on rates, customer experience and coverage breadth.

- ERGO NEXT: Ranked first overall in Minnesota with the highest customer experience score (4.47 out of 5) and the top coverage score among all providers in the state, ERGO NEXT earns its position through a buying process that's straightforward from quote to policy and a coverage structure that works across a wide range of professions. It ranks first in 10 of the 18 industries tracked in Minnesota, including health care, construction, real estate, childcare and pet care. That breadth makes it a strong fit for most Minnesota businesses, regardless of sector. No industries in the state ranked it in the bottom tier.

- The Hartford: The highest affordability score in Minnesota (4.52 out of 5) belongs to The Hartford, and for consulting firms, financial services businesses and hospitality operators, it's the top-ranked provider in the state. With more than 200 years in the industry, it brings dedicated small-business underwriting, risk management resources and a claims team built for professional services work. The one area to watch: health care providers and other professional services businesses will find better-suited options, as The Hartford ranks ninth in both categories for Minnesota.

- Hiscox: Nonprofits and tech businesses in Minnesota get the best fit with Hiscox, which ranks first in both industries statewide. It also ranks second for consulting and financial services, making it a solid option for knowledge-economy businesses across the Twin Cities metro. Hiscox offers coverage to a wide range of professions and a fully online buying experience with support available around the clock.

Ranked providers represent the best fit for most Minnesota businesses, but no single list covers every situation. Comparing business insurance options side by side and pulling quotes directly from multiple carriers gives you a clearer picture of what each policy covers at the price you'll pay.