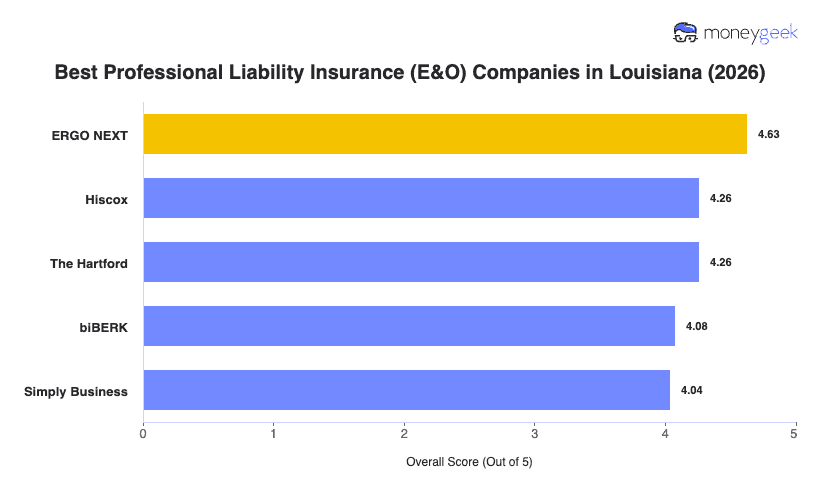

Our analysis of Louisiana professional liability insurers found three providers that consistently outperformed the field on rates, customer experience and coverage quality.

- ERGO NEXT: Affordable rates and a fully digital buying experience earned ERGO NEXT the top spot. It ranks first in 16 of 18 industries in Louisiana, including cleaning, consulting, financial services, health care, real estate and tech. Sole operators and firms under 10 employees will appreciate that coverage, certificates and policy changes are all handled online without a phone call.

- Hiscox: Coverage depth across more than 180 industries and a claims team with high individual resolution authority sets Hiscox apart from most competitors. It ranks first in marketing and communications and hospitality, and second in consulting, financial services, childcare and pet care. Louisiana consultants, financial advisors and creative professionals will find its policy structures a strong fit. Construction and recreation businesses, where it ranks seventh in the state, should compare quotes before committing.

- The Hartford: The ability to bundle professional liability directly into a business owner's policy makes The Hartford a good choice for businesses that want a single consolidated coverage package. It ranks first in arts, media and entertainment, and second in education and tech. Health care providers and other professional services businesses rank it ninth in Louisiana, so those industries should look at other options first.

Ranked providers represent the best fit for most Louisiana businesses, but no list covers every situation. Comparing business insurance options side-by-side and pulling quotes directly from each insurer gives you the clearest picture of what you'll actually pay and what you'll get.