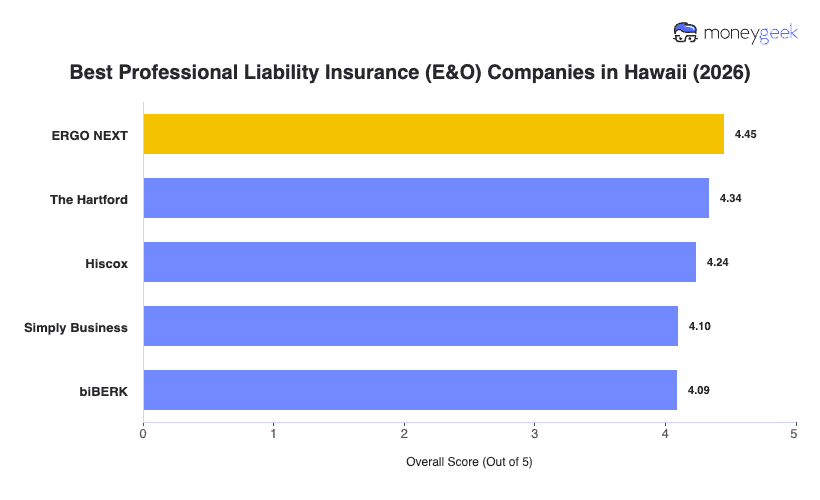

Our analysis of Hawaii professional liability insurers found three providers that consistently outperformed the field on rates, coverage and overall experience.

- ERGO NEXT: A fully digital buying experience and broad industry coverage pushed ERGO NEXT to the top spot in Hawaii. The insurer ranks first across 12 of 18 industries on the island, including healthcare, hospitality, construction, fitness and tech, making it a strong fit for the state's diverse small business mix. Getting a certificate of insurance is instant through the online portal, which matters a lot in Hawaii's contract-heavy tourism and construction markets. Consulting, education and financial services businesses will find better fits elsewhere, as ERGO NEXT ranks toward the bottom of the field in those industries for this state.

- The Hartford: Over 200 years in the industry gives The Hartford a claims handling depth that newer digital-only insurers don't have. It earns the top overall rank in Hawaii for consulting, financial services, education, real estate and cleaning services, and its professional liability policies can be added onto an existing BOP, which keeps things simple if you're bundling coverage. For nonprofits, healthcare and other professional services in Hawaii, the data shows it falls toward the bottom of the field, so those businesses should compare carefully.

- Hiscox: Hiscox built its entire business around small business professional coverage, and it shows in the breadth of what it writes. The insurer covers more than 180 professions and earns second-place rankings in Hawaii across childcare, consulting, financial services, nonprofits, pet care and tech. Its policies are fully customizable and available online, and bundling two or more Hiscox products saves 5% on premiums.

These three providers are the best fit for most Hawaii businesses, but no ranked list captures every situation. Comparing business insurance options side-by-side and getting direct quotes gives you the clearest picture of what you'll actually pay.