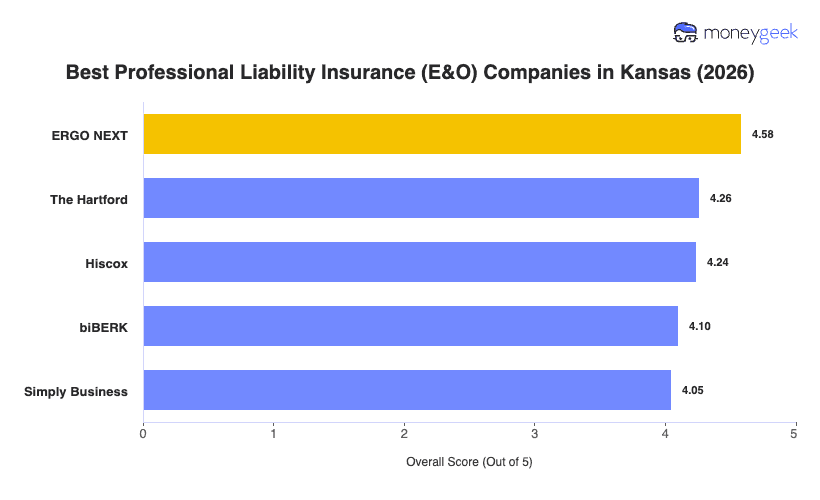

Our analysis of Kansas professional liability insurers found three providers that consistently outperformed the field on rates, coverage quality and service.

- ERGO NEXT: Fully digital from quote to certificate, with a buying process that takes about 10 minutes and no phone calls required. That speed and simplicity earned ERGO NEXT the top spot, backed by rate competitiveness that holds across almost every industry in Kansas, from cleaning services and pet care to construction and financial services. The insurer is backed by Munich Re through its parent ERGO Group, which adds meaningful financial depth behind the policies. Kansas businesses in hospitality should compare closely, as ERGO NEXT ranks fourth in that category in the state.

- The Hartford: A 200-plus year track record gives The Hartford something most competitors can't match: deep institutional knowledge of how professional liability claims actually play out. It earns particularly strong marks for real estate and tech professionals in Kansas, ranking first in both industries statewide. The insurer also allows businesses to bundle professional liability directly into a BOP, which simplifies policy management and can reduce combined premiums. Kansas healthcare providers and other professional services businesses should look elsewhere though, as The Hartford ranks ninth in both of those categories for the state.

- Hiscox: The strongest option in Kansas for nonprofits, financial services firms and consultants, where it ranks first or second statewide. Hiscox writes coverage across more than 180 professions and keeps underwriters who specialize by industry, which shows up in policy terms that are more tailored than what generalist carriers produce. Its claims team operates with high individual authority levels, meaning straightforward claims move faster than at carriers requiring multiple approval layers.

No ranked list covers every situation a Kansas business might have. Comparing business insurance options side by side and getting direct quotes from each carrier gives you the clearest picture of what you'd actually pay and what you'd actually get.