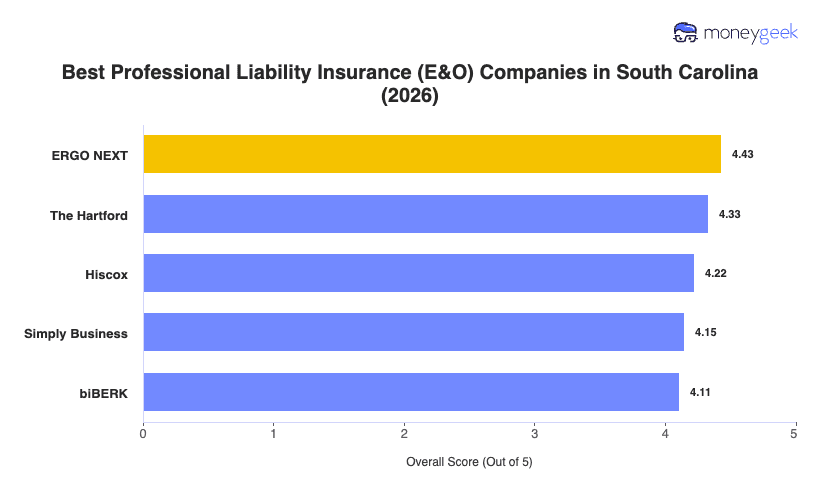

Our analysis of South Carolina professional liability insurers found three providers that consistently outranked the field across affordability, customer experience and coverage quality.

- ERGO NEXT: Broad industry coverage and a buying process that takes about 10 minutes online put this insurer at the top of the South Carolina rankings. ERGO NEXT ranks first across Childcare Services, Construction and Contracting, Fitness, Healthcare and Medical, Nonprofit, Pet Care, Recreation and Sports, and Other Professional Services in the state, a span that makes it the strongest all-around fit for South Carolina's service-driven economy. Education is the one category where the insurer underperforms, so educators should compare other options before committing.

- The Hartford: Financial services, consulting, marketing and real estate professionals get the strongest fit from The Hartford, which ranks first in South Carolina across all four of those industries. The insurer has carried specialized professional liability policies for over 200 years and brings dedicated industry specialists to the process, with the ability to bundle professional liability alongside a business owner's policy for businesses that need multiple coverages under one carrier. Healthcare providers, nonprofits and other professional services firms should look elsewhere, as The Hartford ranks ninth in each of those categories in South Carolina.

- Hiscox: Tech and IT professionals in South Carolina get the best fit from Hiscox, which ranks first in the state for that industry and brings over 120 years of specialist small business underwriting experience to every policy. The insurer covers more than 180 professions and earns strong marks in childcare, fitness, nonprofit and financial services as well, making it a capable option for businesses that want industry-specific coverage depth rather than a one-size-fits-all policy. Construction and contracting and recreation and sports are weaker categories for Hiscox in South Carolina, so businesses in those fields should weigh alternatives.

The three providers above are the best fit for most South Carolina businesses, but no ranked list accounts for every risk profile, budget or coverage requirement your business has. Comparing business insurance options side by side and getting direct quotes gives you the clearest picture of what you'll actually pay and what you'll actually get.