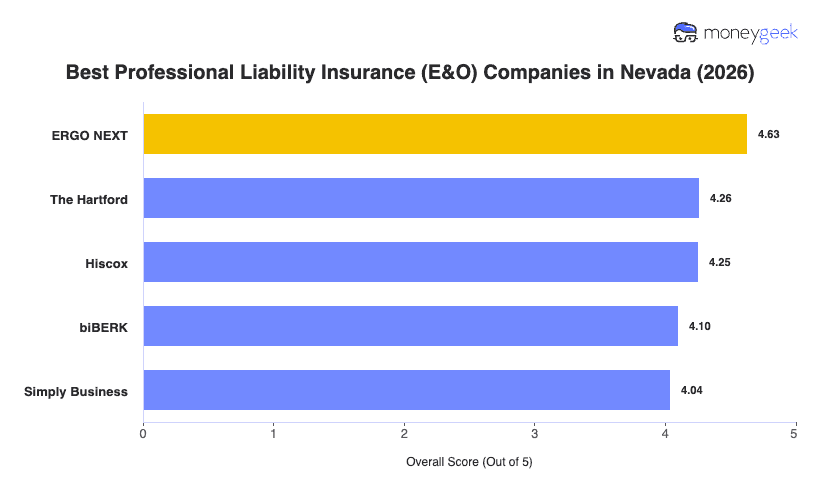

Our analysis of Nevada professional liability insurers identified three providers that outperformed the field across affordability, customer experience and coverage scores.

- ERGO NEXT: Ranked first in overall score across 15 of 18 Nevada industries, with top affordability scores in 14 of those. It's a digital-first carrier built for small businesses, meaning you can get a quote and bind coverage online in minutes rather than waiting days for a broker to come back to you. Nevada cleaning services, fitness studios, childcare providers, consulting firms and healthcare businesses all rank ERGO NEXT at the top of the field. The one segment where it falls behind is hospitality, travel and tourism, where it drops to fourth overall, so Nevada hotel operators and tour companies should compare it carefully against alternatives.

- The Hartford: What earns The Hartford its strong second position is its consistent performance across almost every industry category in Nevada, finishing first in marketing and communications and real estate, and second in education and tech/IT. It brings dedicated specialist support teams and risk management resources that most digital-only carriers don't offer, which matters when you're staring down a professional negligence claim and need more than a chatbot. The one area worth flagging is healthcare and medical in Nevada, where it drops to ninth, so solo practitioners and medical offices should run the numbers on other options before committing.

- Hiscox: Tech/IT is where Hiscox earns its third-place finish outright, ranking first in that category in Nevada, with a strong second in consulting, financial services and childcare. It's been one of the most active small-business E&O carriers in the country and is well-suited to solo practitioners and firms under 10 employees who want a clear digital buying experience. Construction and contracting is its weakest category in Nevada at seventh, so contractors should look at ERGO NEXT or The Hartford first.

The providers ranked here are the best fit for most Nevada businesses, but every business has considerations a ranked list can't fully capture. Comparing business insurance options side-by-side and pulling quotes directly from multiple carriers gives you the full picture before you commit.