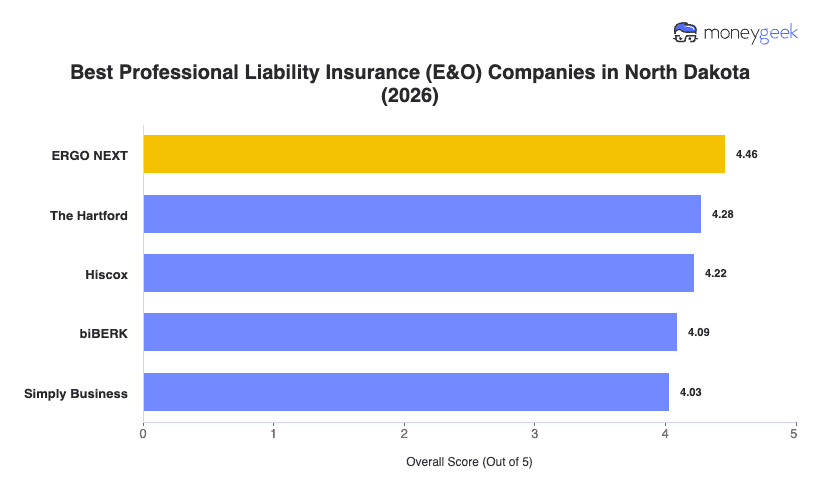

Our analysis of North Dakota professional liability insurers found three providers that consistently outperformed the field on rates, coverage quality and customer experience.

- ERGO NEXT: A fully digital buying experience and some of the sharpest rates in the state earned ERGO NEXT the top spot. You can get a quote, buy a policy and pull a certificate of insurance in under 10 minutes, all without talking to anyone. That kind of speed matters for North Dakota contractors, healthcare businesses and real estate professionals who need to show proof of coverage fast to start a job or close a deal. The insurer ranks first across 13 of 18 industries in North Dakota and has no industry categories where it underperforms.

- The Hartford: Deep claims expertise and a proven track record of quick claims processing set The Hartford apart, particularly for consulting, financial services and tech businesses where North Dakota contract requirements tend to be stricter. It has been writing small business insurance for over 200 years, and its agent-supported buying process is a genuine advantage for businesses with more complex coverage needs who want someone walking them through the details. The insurer does underperform for healthcare and general professional services in North Dakota, so businesses in those categories should compare carefully.

- Hiscox: Purpose-built for small businesses, Hiscox covers more than 180 professions and leads the state for childcare, tech and hospitality professional liability. Its policy terms are thorough, and claims can be reported online or by phone around the clock. North Dakota businesses in wellness, nonprofits and tech will find it particularly competitive on both price and coverage depth.

The providers above are the best fit for most North Dakota businesses, but no ranked list accounts for every situation. Comparing business insurance options side by side and getting direct quotes from each carrier gives you the clearest read on what you'll actually pay and what you'll actually get.