The average cost of retail business insurance for party rental companies runs $157 per month, or $1,888 per year, based on MoneyGeek's analysis of quotes across 50 states and DC. That figure covers the five most common coverage types for a business profile of one to four employees at standard policy limits of $1 million per occurrence and $2 million aggregate.

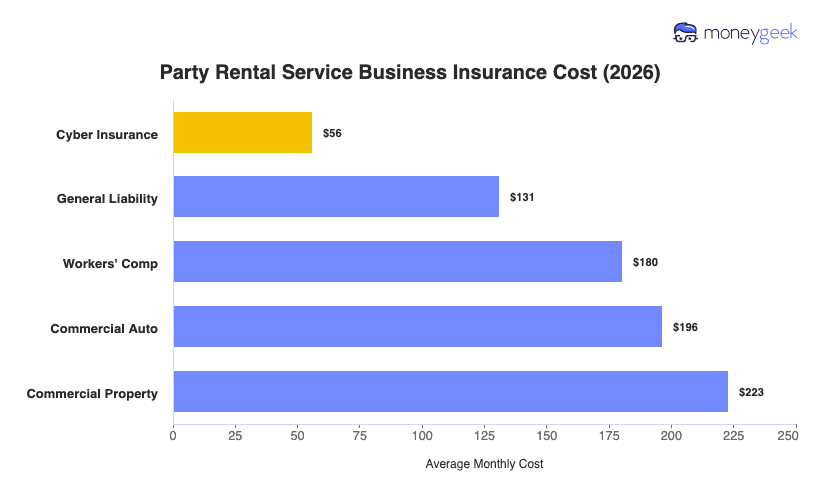

Depending on your policy, your costs can fall between $56 and $223 per month. Cyber insurance is the most affordable coverage type because your primary exposures are physical, such as equipment damage, guest injuries at events and delivery vehicle accidents, not data-related. Commercial property prices highest because your tents, inflatables, generators and linens represent considerable insured value stored in a warehouse and transported to job sites throughout the season.

The coverage breakdown below shows average monthly costs by policy type, but use these figures as starting benchmarks rather than the rate you'll receive, since your actual premium reflects your specific business profile.