The average cost of business insurance for auto repair shops is around $107 monthly or $1,286 annually, based on MoneyGeek's analysis of five coverage types for shops with one to four employees across all states, plus Washington, D.C.

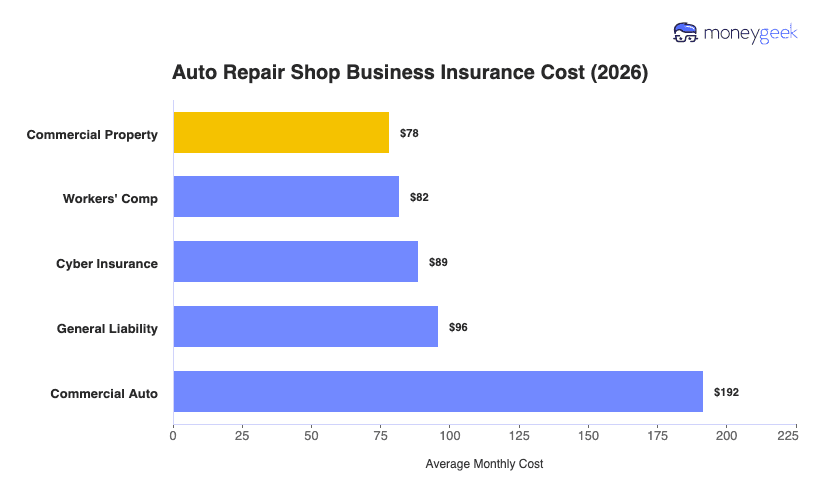

Individual coverage costs range from $78 to $192 per month. Most shops operate from a fixed location, so the building and equipment risk is straightforward to insure. Commercial Auto is the most expensive, since road testing and moving customer vehicles on public roads creates real liability, and insurers price that accordingly, whether your shop does it occasionally or every day.

The table below shows average monthly costs by coverage type. Use these as benchmarks, not quotes, since your actual premium depends on your shop's size, location and operations.