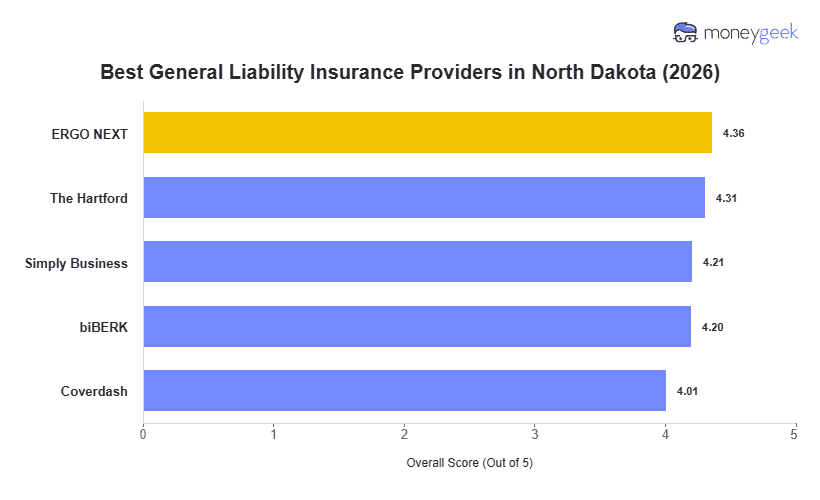

The lowest price doesn't make a general liability policy worth buying. MoneyGeek evaluated 10 insurers across 408 business types in North Dakota to identify the best and cheapest options. These five balance competitive rates with reliable service and flexible coverage:

- ERGO NEXT: Best Overall, Best for Customer-Facing Service Businesses

- The Hartford: Best Cheap General Liability Insurance

- Simply Business: Best for Comparing Multiple Carriers

- biBerk: Best for Active Service Businesses

- Coverdash: Best for Food and Beverage Businesses

Rate breakdowns and rankings for each provider appear in the table below. Contractors bidding on Fargo commercial projects and Main Street retailers in Minot bracing for harsh winter foot traffic will find the cost-versus-coverage details they need to make a call.