Jump to the section that meets your immediate needs best:

Average Barber Shop Insurance Cost (2026 Report)

Barber shop insurance cost average between $96 per month for a starting bundle and $380 for one that fits the coverage needs of a staffed shop.

Your total cost will vary based on the services your offer, how valuable your equipment is, your state and your claims history.

If you want pricing now, MoneyGeek can match you to the insurer that meets your barber shop's coverage needs.

Select state

Updated: July 31, 2026

Advertising & Editorial Disclosure

How Much Does Barber Shop Insurance Cost?

My analysis found that a starting insurance bundle for barbers and barber shops costs an average of $96 per month. It combines general liability with professional liability, which address risks most closely tied to everyday barbering. These include accidents around customers and claims arising from the service you provide, such as customers slipping in the shop, cuts, burns or other injuries caused during an appointment.

If you're an independent barber, booth renter or small owner-operated shop, this bundle could suit your business since you don't have employees and have limited business property. Over time, however, you might need to add coverages to your mix. For example, opening your own shop and purchasing chairs, mirrors, clippers and inventory would create property risks that a starting bundle doesn't cover. I’ve broken the bundles into tiers to help you decide which one fits your barber business.

Starting Bundle | $96 | Solo chair renters or private-suite barbers | |

Recommended Bundle | Business owner’s policy (BOP) + professional liability + equipment breakdown + cyber insurance | $233 | Owner-run shops with one location |

Staffed Shop Bundle | Recommended bundle + workers’ compensation + employment practices liability | $380 | Fixed-location shops with one to four employees |

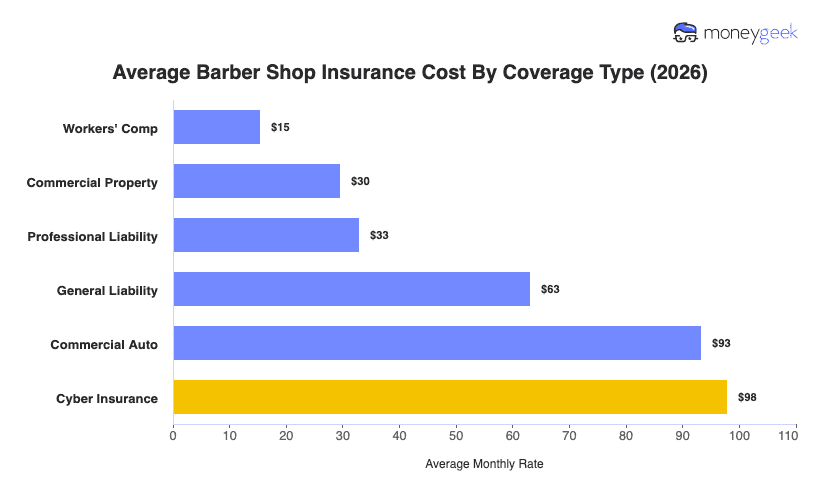

Average Barber Shop Insurance Costs By Coverage Type

While you won't need all the coverages in this list at the same time, these are the most common policies you could include in your policy mix:

- Workers’ compensation: $15 per month ($186 per year)

- Equipment breakdown: $18 per month ($216 per year)

- Commercial property: $30 per month ($354 per year)

- Professional liability: $33 per month ($391 per year)

- General liability: $63 per month ($758 per year)

- Business owner’s policy: $84 per month ($1,001 per year)

- Commercial auto: $93 per month ($1,120 per year)

- Cyber insurance: $98 per month ($1,175 per year)

- Employment practices liability: $132 per month ($1,584 per year)

Remember that bundles are only recommendations, so can always build your own. Choose policies based on the risks your business has. For example, if you're a solo booth renter, general liability and professional liability could be enough. But if you own your shop and have employees, a business owner’s policy to protect the shop and its property and workers’ comp for employee injuries is a better fit.

See what each policy covers and match it to what your business needs to protect. Beyond coverage definitions, I also included state-level analysis for each one so you can see how and why cost estimates vary by location.

Barber Shop Insurance Cost Estimates

Use our business insurance cost calculator and enter your state, coverage type, employee count and vehicle type to estimate insurance costs for a barber shop. Select Get Quotes to compare providers in our network that may fit your business.

Keep these points in mind:

- No personal details are collected or stored

- Workers’ compensation estimates are calculated per employee

- Commercial auto estimates depend on the vehicle type selected

Estimate Barber Shop Insurance Costs

Select Coverage Type

Select State

Select Employee Count

Select vehicle_type

Monthly Rate Estimate—

Select Coverage Type

Monthly Rate Estimate—

Select State

Select Employee Count

Select vehicle_type

Factors Affecting Barber Shop Insurance Costs

Beyond claims history, staffing, location and coverage limits, insurers also look at how you run your shop day to day. These six barber-specific factors can shape the risks they see and the price you pay:

Services offered

Services offeredA basic cut-and-trim menu gives an insurer fewer ways to expect a service-related injury. Add straight-razor shaves, hot towels, colouring or chemical treatments, and you introduce cuts, burns and reactions that push professional liability costs higher.

Chair-rental and contractor arrangements

Chair-rental and contractor arrangementsRenting out chairs changes who’s responsible when something goes wrong. A shop with employees can often insure everyone under one business setup. If you have a chair-rental model, you might need separate coverage from each barber and clearer protection for shared areas.

Mobile and event work

Mobile and event workIf you stay at one insured location, you don’t have to account for tools in transit, accidents during work trips or injuries at unfamiliar venues. Once you start serving clients at homes or events like weddings or pop-ups, you’ll need additional coverages, which increases costs.

Barber equipment and shop systems

Barber equipment and shop systemsThink about what would happen if your hot-water system or wash station stopped working tomorrow. A simple private suite may be able to keep operating after one tool fails, but a larger shop could lose appointments until specialised equipment is repaired or replaced.

Sanitation and infection controls

Sanitation and infection controlsA shop that records blade changes, disinfects clippers between clients and follows consistent cleaning steps presents a different risk from one that handles sanitation informally. Your cleaning process can affect how likely a client is to claim that your service caused an infection.

Retail product sales

Retail product salesSelling products creates responsibilities that don’t end when the appointment does. If you only apply pomade during a service, you have less product exposure than if you sold oils or shampoos in your shop.

How to Lower Barber Shop Insurance Costs

If you're looking for more affordable business insurance, you can apply multiple methods to manage your costs. Some impact your premium before you buy your policy or upon renewal, while others require you to invest more time and effort before you see the effects. You'll get the most if you apply strategies for both timelines.

Compare quotes using the same coverage limits

Compare quotes using the same coverage limitsCompare quotes with the same policies, limits, deductibles and added coverages. A cheaper quote might offer less protection or leave out risks such as professional mistakes or mechanical breakdowns, so the lowest number doesn't automatically mean you're getting the best deal.

Right-size your coverage

Right-size your coverageChoose policies based on how you run your barber business today. A booth renter won't need the same property coverage as a shop owner, the same way you won't need commercial auto insurance if you only work from one location. Make sure you match your coverages with your current risks so you're not paying for financial protection you don't need.

Bundle policies with the same provider

Bundle policies with the same providerA business owner’s policy combines general liability and commercial property coverage, often at a lower cost than buying them separately. But beyond a BOP, insurers also usually give a discount if you get multiple policies from them. This also makes managing your insurance easier since you won't need to deal with several carriers in case of a claim.

Lower your risk profile

Lower your risk profileMonthly payment plans usually include installment or financing fees. Paying the full annual premium upfront can remove some of these charges, though it may not lower the base premium itself. I suggest comparing the total yearly cost of both options rather than focusing only on the monthly payment to see if your savings is worth paying a larger amount upfront.

Invest in risk management practices

Invest in risk management practicesCuts, infections, falls and equipment failures can lead to claims that affect future pricing. I'd focus on controls that address risks built into everyday barbering, since fewer losses may strengthen your renewal options over time. These include:

- Disinfecting clippers and razors between clients to reduce infection claims tied to contaminated tools.

- Drying wet floors, securing loose cords and keeping walkways clear to prevent customer and employee falls.

- Training staff on razor handling, chemical products, hot towels and skin reactions to reduce service-related injuries.

- Servicing water heaters and wash stations regularly so equipment failures are less likely to interrupt appointments or damage the shop.

Barber Shop Insurance Cost: Bottom Line

Your quote makes more sense when you compare it with the bundle built for a business like yours. In my analysis, monthly costs range from $96 for a solo barber with limited coverage needs to $380 for a staffed shop that also needs employee protection. Don't expect your quote to match thee figures exactly, but it's best to understand why it falls above or below the closest comparison.

Use these three questions to put your quote in context:

- Which bundle is closest to how you operate? Start with the business setup that looks most like yours. If you only rent a chair, don't compare your quote with that of a barber who owns a staffed location covering its premises, equipment, digital systems and workers.

- Does your quote include the same coverage as the bundle? A lower price could be leaving out professional liability, cyber insurance, equipment breakdown or employee protection. A higher quote may include more coverage or higher limits, meaning the insurer would pay more toward a covered claim. Look into these before you decide whether a quote is realistic or not.

- Which parts of your business are pushing the price up or down? Opening your own shop, hiring employees, buying essential equipment or using a vehicle for work can move you into a different bundle. I'd the insurer which details had the greatest effect on your price to see if you can do something about it.

Barber Shop Insurance Cost: FAQ

Knowing the estimates that apply to your barber shop and what factors affect it puts you in a better position to gauge if your quote is realistic. That said, you want to clarify other things. I've answered some frequently asked questions barbers might have about their insurance costs below:

Barber shop insurance costs depend on the bundle you need. Based on my analysis, a starting bundle averages $96 per month, a recommended bundle averages $233 per month and a staffed shop bundle averages $380 per month. I’d compare your quote with the bundle that most closely matches your setup, then check whether it includes the same policies, limits and deductibles.

Not always. Employees are usually covered through the shop’s business policies, while independent barbers and chair renters might need their own liability coverage. Check how each worker is classified and read the shop agreement before assuming one policy covers everyone. I’d also confirm this directly with the insurer, since coverage for independent contractors can vary.

A shop owner’s policy may protect the business and shared areas without covering every claim tied to a booth renter’s services. Booth renters often need their own general and professional liability insurance for injuries or mistakes connected to their work. Review the rental agreement and ask your insurer whether independent barbers are included, excluded or required to carry separate coverage.

Commercial property insurance covers tools while they're in your shop, but your policy's protection won't extend to when you take them elsewhere. Tools and equipment coverage can follow clippers, trimmers and other portable gear to clients, events or temporary workspaces. Check the policy’s theft rules, location limits and vehicle exclusions before relying on it away from the shop.

A personal auto policy won't cover regular mobile appointments or a vehicle owned by your barber business. When you request for a quote, tell your insurer how often you drive for work and what you carry. Commercial auto usually fits business-owned vehicles, while hired and non-owned auto may suit occasional use of personal, rented or employee-owned cars.

How We Determined Barber Shop Insurance Costs

We modelled barber shop insurance costs around the points where a barber’s day-to-day operation creates a new type of exposure. The estimates draw on pricing from 10 major U.S. commercial insurers and follow a progression from a solo barber to a fixed-location shop and then to a staffed business with broader responsibilities.

- National benchmark average: We used small barber businesses with fewer than five employees to create the national cost estimates. Each profile only includes the coverage that fits how it operates. A solo barber needs protection for customer accidents and service-related claims, while a dedicated shop also has furniture, equipment and digital systems to insure. Hiring employees adds workers’ compensation and employment practices liability once payroll and workplace decisions become part of the business.

- State averages: To isolate the effect of location, we kept the barber shop profile the same in every state. The services offered, payroll, staffing, equipment value, policy limits and other business details did not change. For specialised coverages outside the main dataset, we started with the national estimate and adjusted it using the state pattern of the most closely related policy.

- Bundle averages: The bundles reflect recognisable barber business setups rather than simply adding more policies at each level. The starting bundle suits a solo barber or chair renter focused on customer and service claims. The recommended bundle fits an owner-run shop with a permanent location, business property and digital systems. The staffed shop bundle adds the coverage tied to employees and workplace claims.

Use these figures as a budgeting benchmark rather than a prediction of your final quote. Your price can still change based on the services you offer, whether you rent chairs, the value of your tools and equipment, your use of mobile or event work, sanitation practices, product sales, location and the limits, deductibles and policy terms you choose.

See our full business insurance methodology.

About Angelique Palenzuela-Cruz

Angelique Palenzuela-Cruz is a Business Insurance Content Writer at MoneyGeek, where she specializes in general liability, workers’ compensation and professional liability insurance. Her work helps small business owners understand how these policies apply to coverage, including risks like customer injuries, employee injuries, professional mistakes, client contract terms and industry-specific coverage requirements.

She primarily covers service-based businesses where liability and employee coverage decisions are especially important, including cleaning, consulting, beauty and wellness, childcare, education, fitness, food service, pet care, repair and maintenance, and other professional services.

Before joining MoneyGeek, Angelique spent nearly 12 years at Guthrie-Jensen Consultants, one of Southeast Asia’s largest management training firms, where she advanced from Training Consultant to Managing Consultant. In that role, she worked with business clients to assess operational needs, develop training programs and present performance analyses to executive decision-makers. She also helped establish Gladwin Training Consultancy, where she served in learning solutions and client service roles.

Her background gives her practical context for writing about how businesses operate, manage client expectations, structure teams and make risk decisions. At MoneyGeek, she applies that experience to business insurance content, connecting coverage to actual business needs.

LinkedIn: linkedin.com/in/ma-angela-cruz

Email Contact: angelique.palenzuela@moneygeek.com

Sources

- California Department of Forestry and Fire Protection. "Statistics." Accessed August 5, 2026.

- California Department of Industrial Relations. "DWC Announces Temporary Total Disability Rates for 2026." Accessed August 5, 2026.

- Federal Bureau of Investigation, Internet Crime Complaint Center. "2025 IC3 Annual Report." Accessed August 5, 2026.

- Michigan Department of Insurance and Financial Services. "Auto Insurance Reform FAQ." Accessed August 5, 2026.

- Michigan Department of Insurance and Financial Services. "Frequently Asked Questions." Accessed August 5, 2026.

- Pennsylvania Insurance Department. "Auto Insurance." Accessed August 5, 2026.

- U.S. Bureau of Economic Analysis. "Regional Price Parities by State and Metro Area." Accessed August 5, 2026.

- U.S. Fire Administration. "Preliminary After-Action Report: 2023 Maui Wildfire." Accessed August 5, 2026.

- Workers’ Compensation Insurance Rating Bureau of California. "WCIRB Releases 2025 State of the California Workers’ Compensation Insurance System Report." Accessed August 5, 2026.