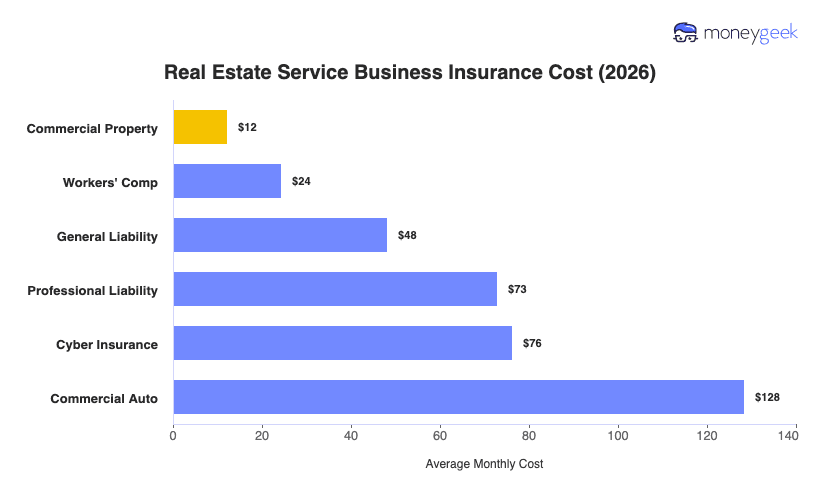

Your real estate business insurance averages $60 per month, or $724 per year, across the six most common coverage types. That reflects the average cost of business insurance for businesses with one to four employees, modeled across 50 states and D.C. at $1 million per occurrence and $2 million aggregate.

Depending on what you carry, your individual policy costs range from $12 to $128 per month. Commercial property tends to sit at the low end if you work from a small office or remotely, while commercial auto runs highest when your agents drive to showings, inspections and client sites. The figures below are benchmarks, not quotes, and your actual premium depends on your specific profile.