Plumbing contractors pay an average of $189 per month, or $2,269 per year, across the six most common coverage types. MoneyGeek's analysis of business insurance cost for contractors ranks plumbing 20th out of 45 subindustries on affordability, and covers businesses with one to four employees across all 50 states and Washington, D.C., using policy limits of $1 million per occurrence and $2 million aggregate, with 16 vehicle types modeled for commercial auto.

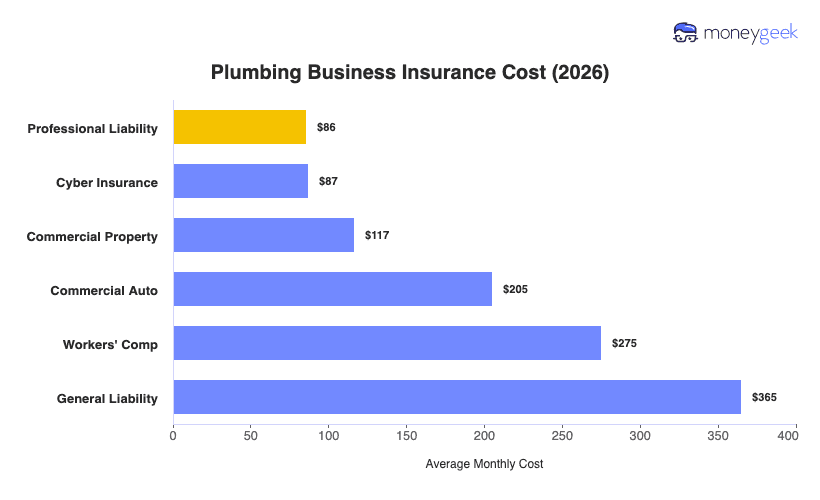

Individual coverage types run from $86 to $365 per month, with professional liability sitting at the low end because most plumbing work is physical and hands-on, which limits the professional error exposure that policy addresses. General liability lands at the top, which reflects the cost of working inside client properties where a failed connection or an overflowing drain can quickly become a third-party property damage claim.

The table below shows the average monthly figure for each coverage type, though your actual premium varies with your employee count, location and claims history.