The cost of retail business insurance for bounce house rentals averages $138 per month or $1,662 per year, across five coverage types. That figure reflects businesses with one to four employees, standard policy limits of $1 million per occurrence and $2 million aggregate, and operations across all 50 states and Washington, D.C.

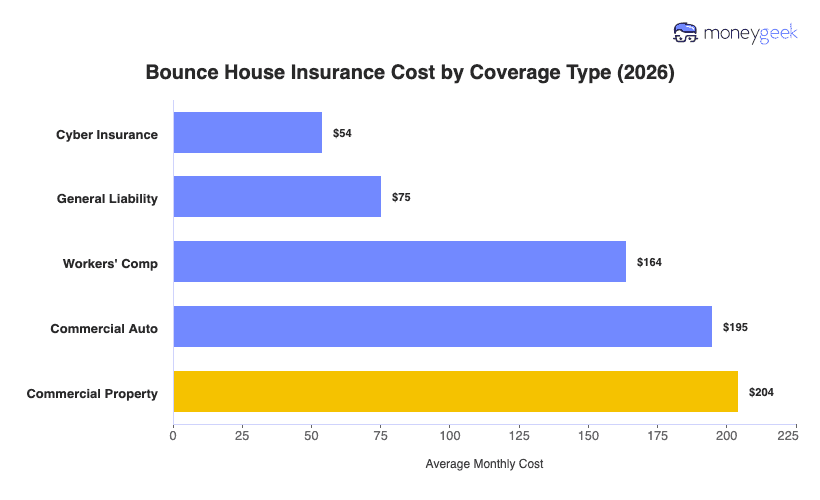

Within the retail and product rental category, bounce house operations rank 25th out of 35 on affordability, which means most retail segments price lower. At the individual policy level, the range runs $54 to $204 per month. Cyber insurance sits at the low end at $54, reflecting the relatively narrow online exposure most operators carry, like booking software and payment processing. Commercial property reaches $204, driven by the replacement cost of owned inflatable inventory: a single commercial-grade unit runs $3,000 to $8,000, and most operators carry several.

Use the table below as a benchmark for your planning as your actual premium will vary based on your business profile.