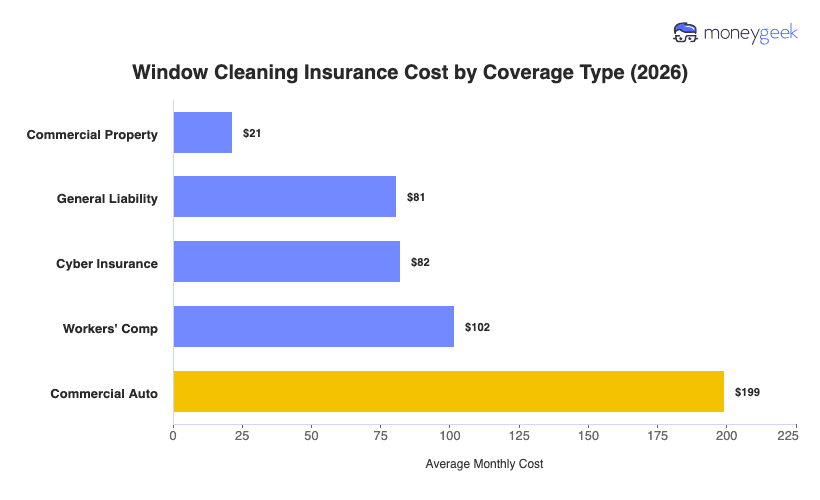

The cleaning business insurance cost for window cleaning averages around $97 a month, or roughly $1,165 a year. That figure reflects an average across five coverage types analyzed for window cleaning businesses with one to four employees, using standard policy limits of $1 million per occurrence and $2 million aggregate across all 50 states and D.C.

Individual policy costs run from around $21 to $199 a month depending on the coverage type. Commercial property sits at the low end because you typically work out of client locations, not owned premises, so your fixed property exposure stays minimal. Commercial auto costs the most because if you have service vehicles, they carry crews, water-fed poles and ladders, and personal auto policies don't cover that kind of use.

The figures below are benchmarks, not quotes as your actual premium varies with your crew size, vehicle count and coverage selections