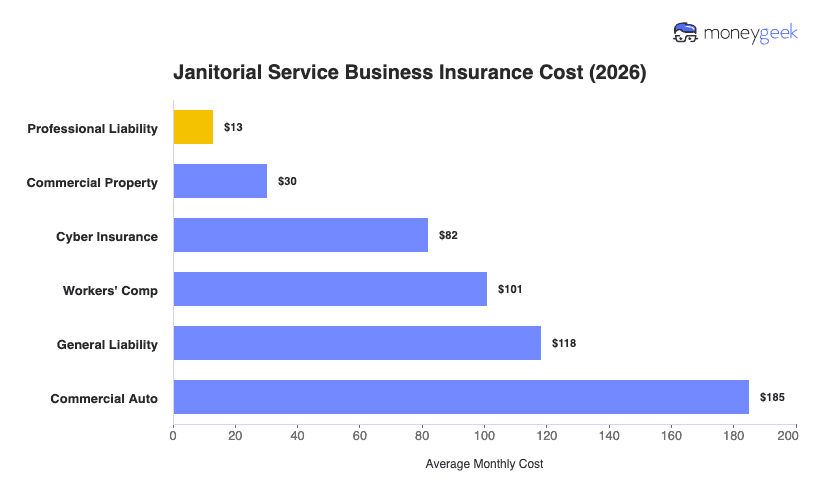

Cleaning business insurance costs for janitorial services average around $88 per month, or about $1,059 per year, across the six most common coverage types. MoneyGeek modeled this across 50 states and Washington, D.C., for businesses with one to four employees at standard policy limits.

What you pay for a single coverage type ranges from $13 per month for professional liability to $185 per month for commercial auto. Professional liability prices low because your claims are far more likely to involve a damaged client floor or a slip-and-fall than a professional error. Commercial auto runs highest because your crews drive to every job and your vans haul equipment and chemical supplies to each site.

Use the figures in the table below as benchmarks, not quotes as you actual premium depends on your payroll, crew size and the clients you serve.