The average welding contractor and shop insurance cost averages $233 per month or $2,792 per year, across the five common coverage types, and sits at the lower end of the construction businesses insurance costs. If your business has one to four employees, operates locally or across state lines and carries standard limits of $1 million per occurrence and $2 million aggregate, that figure gives you a starting point to compare your quote.

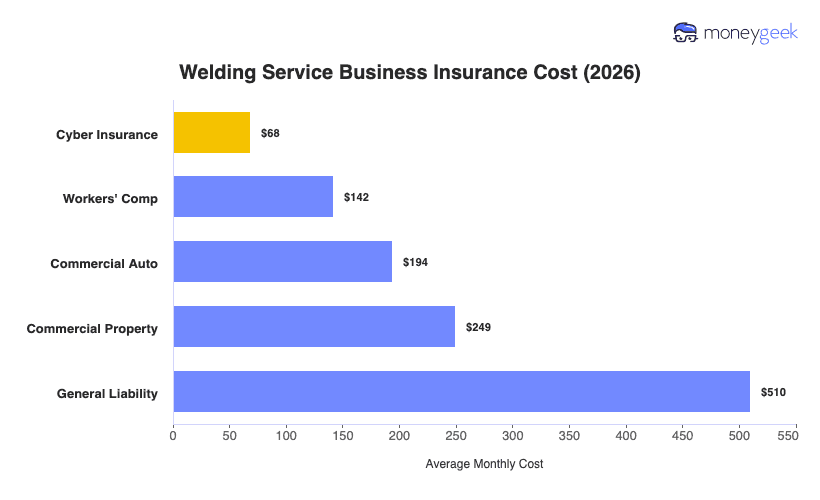

At the individual policy level, your costs can range from $68 to $510 per month depending on which coverage types your operation requires. Cyber insurance sits at the low end because most welding businesses carry limited digital exposure, which keeps that premium relatively contained. General liability has the highest estimate, which reflects the burn and fire hazards that follow hot work into every job site, plus the structural liability risk if fabricated components fail.

The table below shows average monthly premiums by coverage type, but treat those figures as benchmarks rather than quotes, since your actual premium will vary based on your trade, payroll, location and claims history.