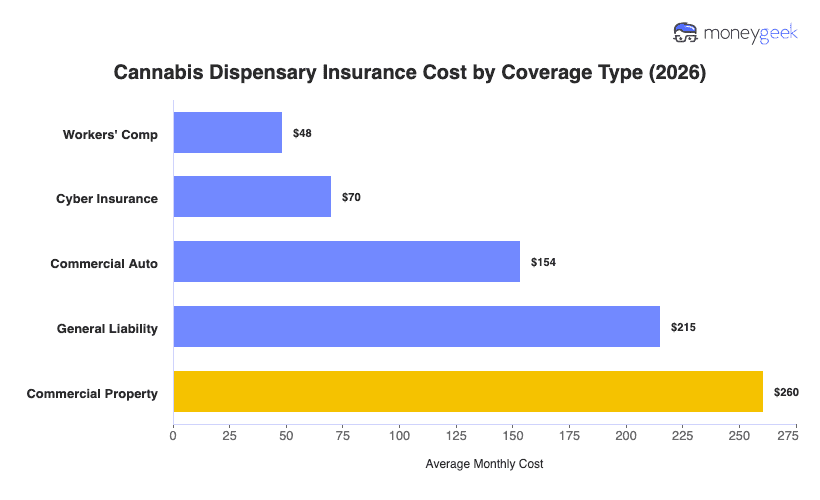

Retail business insurance costs for cannabis dispensaries average around $150 per month, or about $1,795 per year across five coverage types, 35% above the industry average and the most expensive across sub-industries in the retail category. Most mainstream insurers won't cover cannabis businesses, so your options sit in a specialty market where general liability and commercial property rates run higher than what a conventional retailer would pay.

Your coverage type breakdown tells a split story. Workers' comp is the most accessible policy in your stack, pricing 57% below the industry average because the retail classification carries lower injury risk than cultivation or manufacturing. Commercial property sits at the other end once you account for finished stock coverage, since standard property policies exclude cannabis inventory by default. The table below gives you a benchmark for each coverage type, though your actual premium will vary based on your specific business profile.