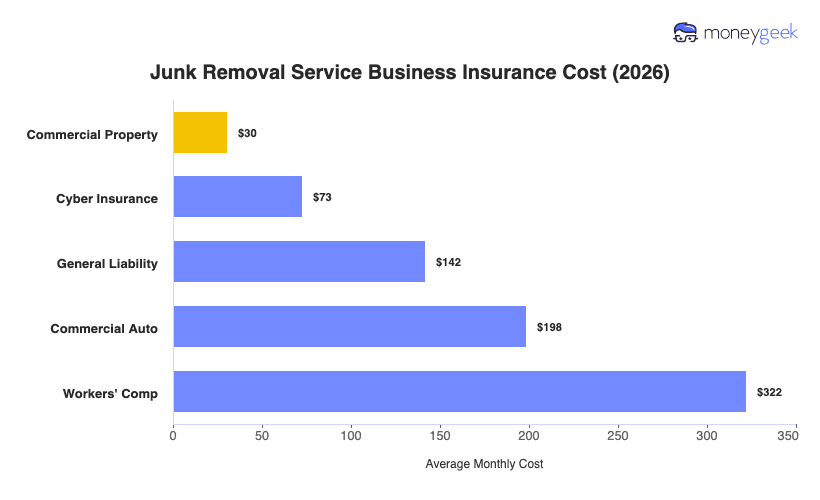

The cleaning business insurance cost for junk removal runs around $153 per month, or about $1,837 per year, averaged across the five coverage types, though that figure covers junk removal companies with one to four employees, policy limits of $1 million per occurrence and $2 million aggregate, across 50 states and Washington, D.C.

Individual policy costs range from around $30 per month to $322 per month. Commercial property prices low because most junk removal businesses don't own commercial real estate. Workers' compensation prices highest because your crew is rink injuring themselves from the heavy lifting, loading and unloading.

The figures below are benchmarks, not quotes, since your actual premium depends on your payroll, fleet size and the jobs you take on.