Our analysis of Rhode Island professional liability insurers found three providers that consistently outperformed the field on rates, service quality and coverage fit across the state's major industries.

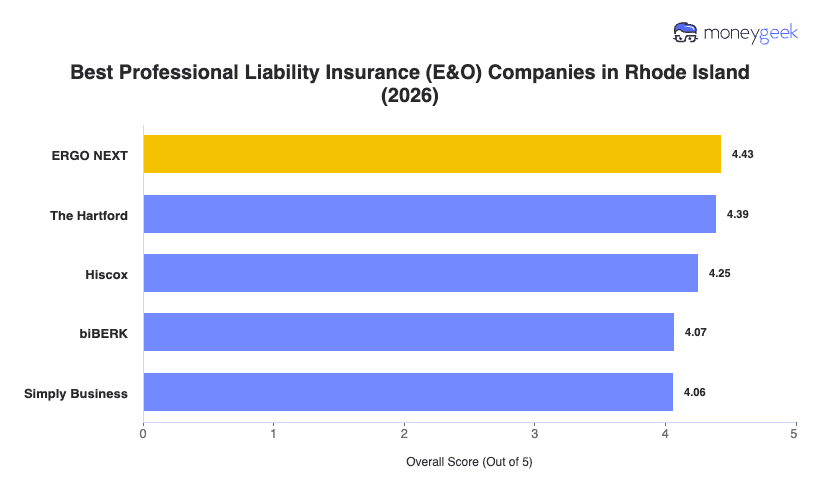

- ERGO NEXT: Breadth of industry coverage combined with a fast, fully digital buying experience earned ERGO NEXT the top spot in Rhode Island. It ranks first across more industries than any other provider in the state, including tech, healthcare, construction, marketing and nonprofits, making it a strong fit for most Rhode Island businesses regardless of sector. The insurer's online quoting process is built for small and mid-size businesses that want coverage without spending hours on the phone.

- The Hartford: Over 200 years in business gives The Hartford a depth of profession-specific expertise that newer digital insurers can't match, particularly for Rhode Island's financial services firms, real estate professionals, consultants and tech companies, where it ranks first or second. It's worth noting that healthcare providers and other professional services businesses in Rhode Island will find better-ranked options elsewhere, as The Hartford places ninth in both of those categories for the state.

- Hiscox: Childcare providers, nonprofits, consultants and financial services businesses in Rhode Island will find Hiscox's coverage options particularly well-suited to their needs, with first or second-place rankings across all of those industries. The insurer also offers 24/7 online access to policies and dedicated support lines for small business owners who want to manage their coverage without going through a broker.

Ranked providers represent the best fit for most Rhode Island businesses, but no single list captures every consideration your business has. Comparing business insurance options side-by-side and getting quotes directly from carriers gives you the clearest picture of what's right for your situation.