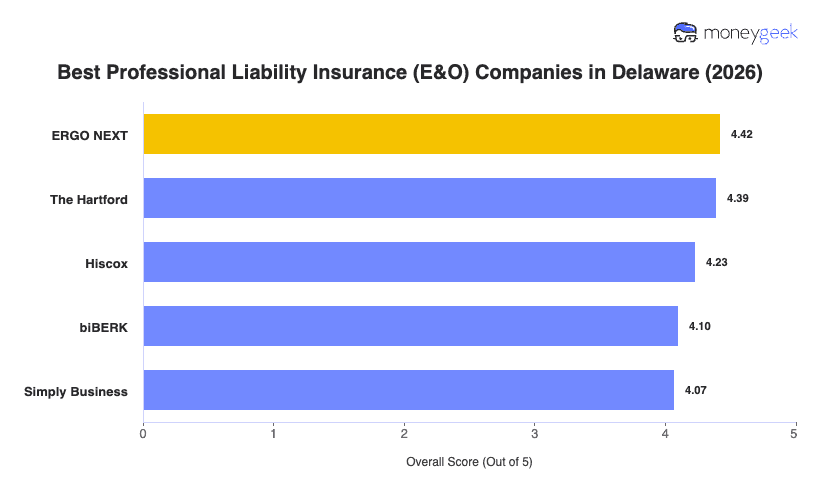

Our analysis of Delaware professional liability insurers found three providers that consistently outperformed the field on rates, service quality and coverage across the state's most common business types.

- ERGO NEXT: A fully digital buying experience, broad profession coverage across more than 1,300 business types and strong scores across both customer experience and coverage breadth put ERGO NEXT at the top of the Delaware rankings. It ranks first for healthcare, tech, construction, fitness, pet care and several other industries in the state. Financial services and consulting businesses will find better rates and a stronger coverage fit with The Hartford, which outperforms ERGO NEXT in both of those categories for Delaware.

- The Hartford: Financial services, consulting, marketing and real estate professionals in Delaware get their strongest overall fit here, with The Hartford earning the top affordability score of any provider in the state. With more than 200 years in business, it brings the ability to bundle professional liability into a broader business owner's policy and offers online claims filing around the clock. Healthcare and other professional services businesses are the exception, as The Hartford ranks near the bottom for those two categories in Delaware.

- Hiscox: Built specifically for small businesses, Hiscox covers professionals across more than 180 industries and lets you buy, manage and update your policy entirely online. Its customer service line runs 7 a.m. to 10 p.m. ET on weekdays, which is useful when you need a live person before a contract deadline. No single industry in Delaware ranks in Hiscox's weak zone, making it a reliable fallback if the top two don't fit your profession.

These three providers cover most Delaware businesses well, but no ranked list accounts for every profession, coverage need or budget. Comparing business insurance options side by side gives you a clearer read on which carrier fits your actual situation.