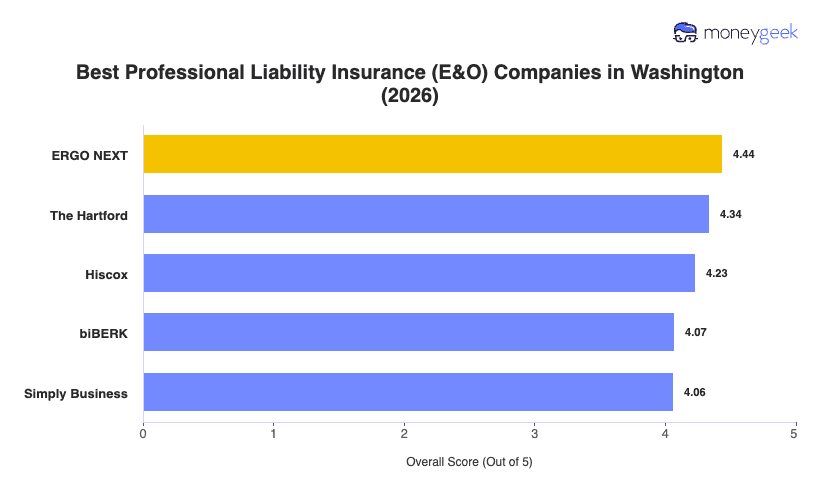

Our analysis of Washington professional liability insurers found three providers that consistently outperformed the rest on affordability, customer experience and coverage breadth.

- ERGO NEXT: An entirely online buying process that takes roughly 10 minutes from quote to bound policy earned ERGO NEXT the top position in Washington. The insurer ranks first in overall score across 11 of 18 industries tracked in the state, including healthcare, marketing, nonprofits, real estate, construction and pet care. Certificates of insurance are available instantly through the ERGO NEXT app or web dashboard, which suits Washington businesses that need to show proof of coverage quickly for client contracts or government work.

- The Hartford: Depth of profession-specific underwriting sets The Hartford apart as the second-ranked option in Washington. It ranks first in the state for both consulting services and financial services, and second across arts and media, cleaning services, hospitality, marketing and real estate. The Hartford's professional liability policies include retroactive dates and extended reporting period options built into the policy structure, which gives Washington businesses added flexibility when switching carriers or winding down operations.

- Hiscox: Coverage depth across a wide range of industries, backed by specialized underwriting teams for each sector, puts Hiscox at third overall in Washington. It ranks first in hospitality and travel as well as tech/IT, and second in consulting and financial services. Hiscox has operated for more than 125 years and carries an A (Excellent) financial strength rating, and its professional liability policies can be bundled with cyber coverage, a pairing that matters for Washington's large tech and financial services workforce in the Seattle and Bellevue corridors.

These three providers represent the best fit for most Washington businesses, but no ranking accounts for every variable your business brings to the table. Comparing business insurance options side by side and getting direct quotes from each insurer gives you a clearer read on which coverage structure and price point actually fit your operation.