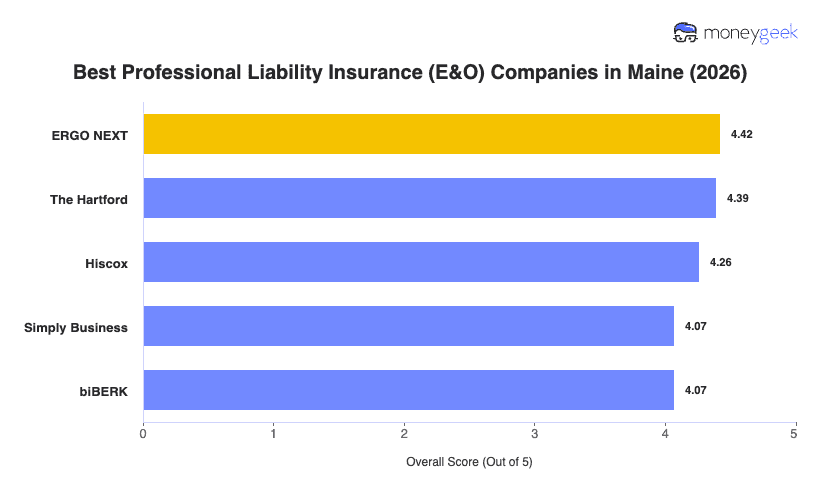

Our analysis of Maine professional liability insurers found three providers that consistently outperformed the rest on affordability, coverage quality and customer experience.

- ERGO NEXT: Instant quotes, a fully digital buying process and a certificate of insurance you can download the moment coverage activates earned ERGO NEXT the top spot. It ranks first in Maine across arts and media, childcare, construction, fitness, pet care, recreation and other professional services, making it a strong fit for hands-on businesses and service providers that need to move fast on coverage. Prior acts coverage is also available for businesses switching from another carrier.

- The Hartford: Coverage for professionals across more than 60 industries, combined with dedicated specialist support and strong claims processing, puts The Hartford in a clear second. It's the strongest option in Maine for consultants, financial services firms, marketing agencies and hospitality businesses. Note that professional liability quotes require a phone call rather than an online application, so build in extra time if you're shopping close to a contract deadline.

- Hiscox: With roots in Lloyd's of London and more than a century of specialist underwriting behind it, Hiscox writes broader E&O policy forms than most small-business carriers. It's the top-ranked option in Maine for tech and IT professionals and nonprofits, and its policies are available to buy online around the clock.

These three providers cover the majority of Maine businesses well, but no ranked list accounts for every situation. Comparing business insurance options side by side and getting direct quotes gives you the clearest picture of what each insurer will actually charge your business.