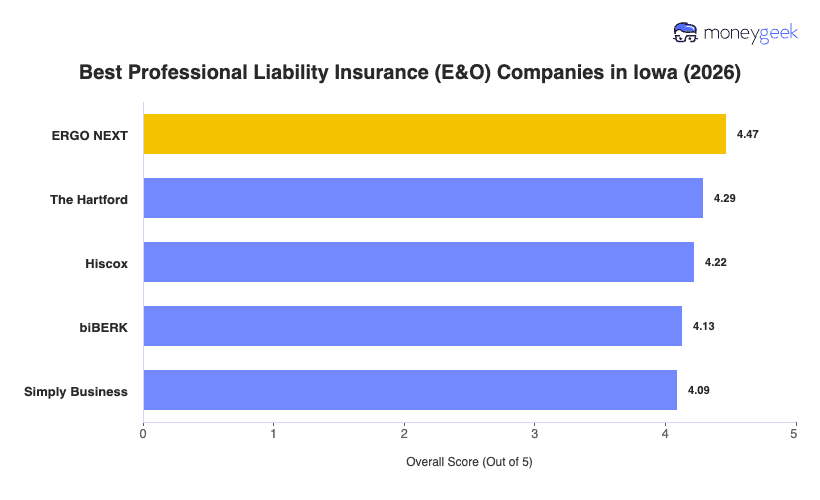

Our analysis of Iowa professional liability insurers found three providers that consistently outperformed the field on affordability, coverage quality and customer experience across the state's major industries.

- ERGO NEXT: A fully digital buying experience, 24/7 policy servicing and the ability to get covered in around 10 minutes put it at the top for Iowa businesses that want to move fast without sacrificing coverage. It ranks first overall in 13 of 18 Iowa industries, including health care, tech, construction, cleaning, fitness, pet care and childcare. The insurer doesn't perform as well in consulting, financial services, education or hospitality, where other providers take the top spot.

- The Hartford: Deep specialization in financial services and consulting gives The Hartford a clear edge for Iowa's financial advisors, CPAs and Des Moines-area consulting firms, where it ranks first overall in the state. It's been writing commercial insurance for more than 200 years, and that depth shows in coverage breadth and a complaint index that runs 22% below the national average for its size. Health care and other professional services are where it falls off, ranking ninth in Iowa for both categories.

- Hiscox: A century-plus of specialty insurance experience and coverage tailored across more than 180 professions make it a good fit for Iowa businesses that don't fit a standard mold. It ranks well for beauty and wellness, childcare and hospitality. The buying process is fully online, and its industry-specific policy language tends to be more detailed than generalist competitors.

Ranked providers are the best fit for most Iowa businesses, but rankings can't account for every situation. Comparing business insurance options side-by-side and pulling quotes directly from multiple carriers gives you the clearest picture of what's right for your business.