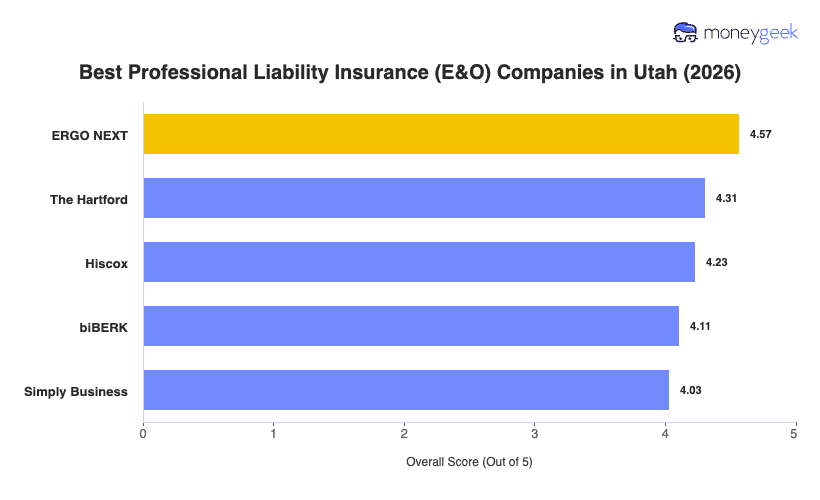

Our analysis of Utah professional liability insurers found three providers that consistently outperformed the field on affordability, customer experience and coverage breadth.

- ERGO NEXT: Topping the Utah rankings came down to two things: rate competitiveness across nearly every industry and a buying experience that takes about 10 minutes from start to finish, entirely online. The insurer ranks first for both affordability and customer experience in Utah and leads on price across 15 of 18 industries, including consulting, financial services, cleaning, fitness, pet care and construction. Utah businesses in education should look elsewhere, as ERGO NEXT's rates for that industry come in above the state average, and its overall rank there drops to seventh.

- The Hartford: A broad industry appetite and an agent-assisted buying process set The Hartford apart from the fully digital options in this ranking. It earns the top spot in Utah for hospitality, travel and tourism businesses, and its coverage structure suits small and mid-size firms that want a licensed agent to walk them through policy limits and coverage options rather than buying online. The insurer has built a track record of low complaint volume relative to its market size, which matters when you actually need to use the policy.

- Hiscox: Depth of industry specialization is what earns Hiscox the third spot. The insurer covers architecture, engineering, consulting, health care, financial services and nonprofit organizations with policies built around the specific claim types those professions see, not a one-size-fits-all E&O form. It ranks in the top two for consulting, financial services, nonprofit and childcare in Utah. Businesses that want coverage customized to their profession rather than a standard policy will find more flexibility here than with most competitors.

These three providers fit the needs of most Utah businesses, but no ranked list accounts for every situation your business is in. Comparing business insurance options side-by-side and getting direct quotes gives you a clearer read on which insurer works best for your profession and contract requirements.