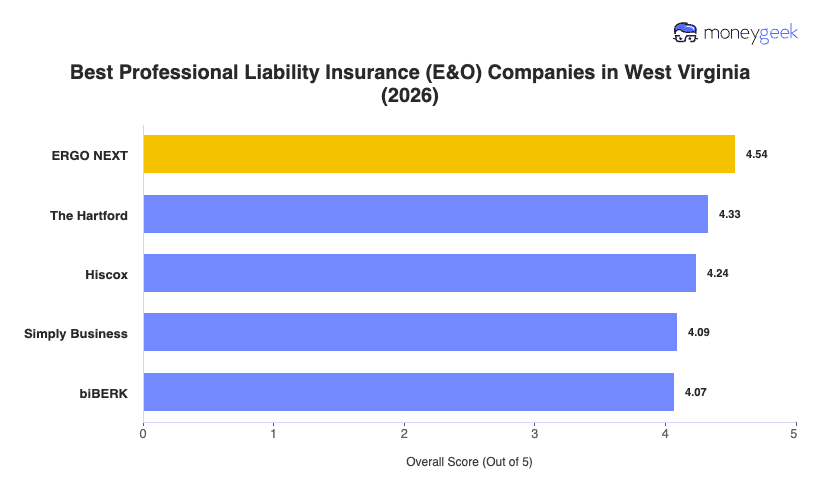

Our analysis of West Virginia professional liability insurers found three providers that consistently outperformed the rest on rates, coverage quality and customer experience.

- ERGO NEXT: Part of Munich Re's ERGO Group, it brings the buying speed of a pure digital insurer with the financial backing of one of the world's largest reinsurance networks. The entire process, from quote to certificate of insurance, runs online without a phone call, which matters for West Virginia contractors, consultants and healthcare businesses that need to move fast. It ranks first in West Virginia across 13 of 18 industries and carries no industry exclusion caveats from our data. Businesses in education should look elsewhere, where it ranks 7th in the state.

- The Hartford: Its claims-handling depth and agent-supported buying process suit West Virginia businesses that want a licensed professional walking them through coverage decisions rather than figuring it out alone online. It earns top marks in the state for real estate and education professionals. Healthcare and other professional services businesses will find stronger fits elsewhere, as The Hartford ranks 9th for both in West Virginia.

- Hiscox: Its professional liability policies cover more than 180 specific industries, making it the right call for West Virginia nonprofits, financial services firms and tech businesses that need coverage built for their specific work. Its E&O forms run broader than what most mass-market carriers offer, and its coverage depth is hard to match at the small-business level.

The three providers above suit most West Virginia businesses well, but no ranked list covers every situation. Comparing business insurance options side by side and getting quotes directly gives you the clearest picture of what fits your business.