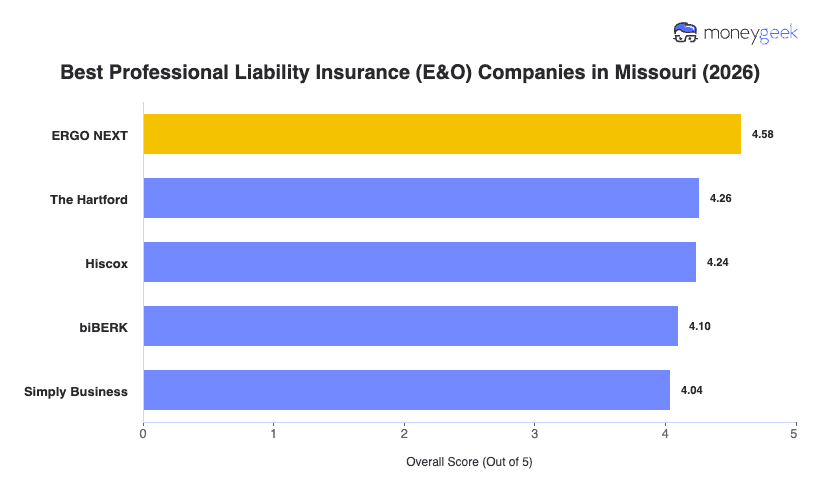

Our analysis of Missouri professional liability insurers found three providers that outperformed the field on combined affordability, customer experience and coverage breadth.

- ERGO NEXT: A fully digital buying experience means Missouri businesses can get a quote, bind coverage and pull a certificate of insurance without calling anyone or waiting on paperwork. ERGO NEXT ranks first in Missouri across 16 of 18 industries for overall score, making it the most broadly applicable option in the state. The insurer is especially well-suited to solo operators and businesses with fewer than 10 employees, where its streamlined policy structure works as a genuine strength, not a drawback.

- The Hartford: More than 200 years in business translates into claims handling infrastructure that smaller digital carriers don't have, and Missouri businesses in education, arts and media, hospitality and marketing consistently rank The Hartford among their best options. The insurer works through agents rather than offering full online binding, giving businesses a human touchpoint during purchase when they want guidance on coverage structure. It ranks ninth for health care and other professional services in Missouri, so medical practices and general professional services firms will find better fits elsewhere on this list.

- Hiscox: Industry specialization is where Hiscox earns its spot, ranking second in Missouri for consulting, financial services, tech/IT, nonprofits and childcare. Its underwriting teams focus on professional categories instead of treating every small business the same, and its online quote and buying process runs 24 hours a day. Missouri businesses in consulting, financial advice and technology services get coverage terms particularly well-matched to what they actually do.

These three providers suit the large majority of Missouri businesses, but no ranked list captures every variable your operation brings. Comparing business insurance options and getting direct quotes from multiple carriers gives you the most complete picture before committing to a policy.