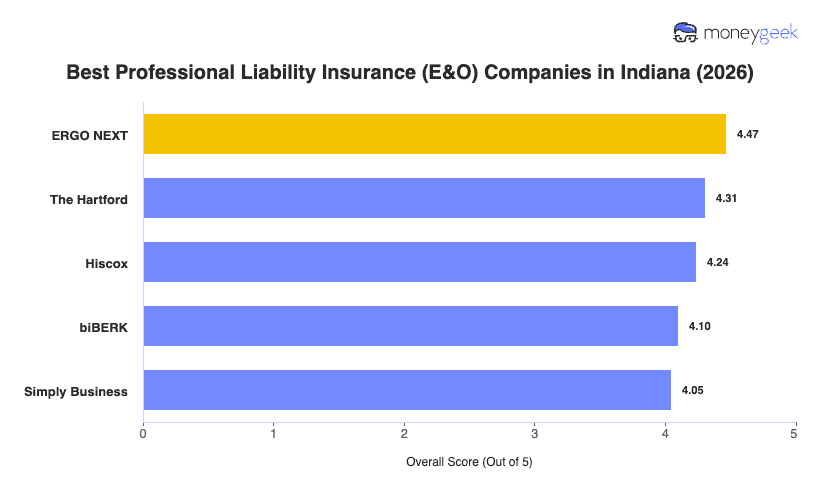

Our analysis of Indiana professional liability insurers found three providers that consistently outperformed the field on affordability, coverage breadth and customer experience.

- ERGO NEXT: Ranking first across 13 of 18 industries in Indiana, it earns its top spot through a fully digital buying experience that gets most small businesses covered in about 10 minutes, with instant certificate of insurance access through its mobile app. The insurer suits hands-on businesses particularly well, including healthcare providers, contractors, fitness businesses, childcare providers and cleaning services. Consulting firms and financial services businesses in Indianapolis should compare options before committing, as ERGO NEXT ranks sixth in both of those industries in Indiana.

- The Hartford: Deep profession-specific coverage options set The Hartford apart, earning it the top rank for consulting, financial services, real estate and tech businesses in Indiana. With more than 200 years in the business, it brings dedicated specialist support and the ability to bundle professional liability into a broader business owner's policy, which is useful for Indiana businesses that want their coverage consolidated with one carrier. Healthcare and other professional services are its weaker spots in the state, where it ranks ninth.

- Hiscox: Broad industry reach and specialist underwriting make Hiscox a strong fit for Indiana businesses in wellness, nonprofits, financial services and consulting, where it ranks second statewide. The insurer handles its own claims in-house with profession-specific support staff rather than routing to generalist adjusters, which matters when a negligence claim gets complicated.

Ranked providers represent the best fit for most Indiana businesses, but no single list covers every situation. Comparing business insurance options side-by-side and getting quotes directly from multiple carriers gives you the clearest picture of what you'll actually pay and what you'll actually be covered for.