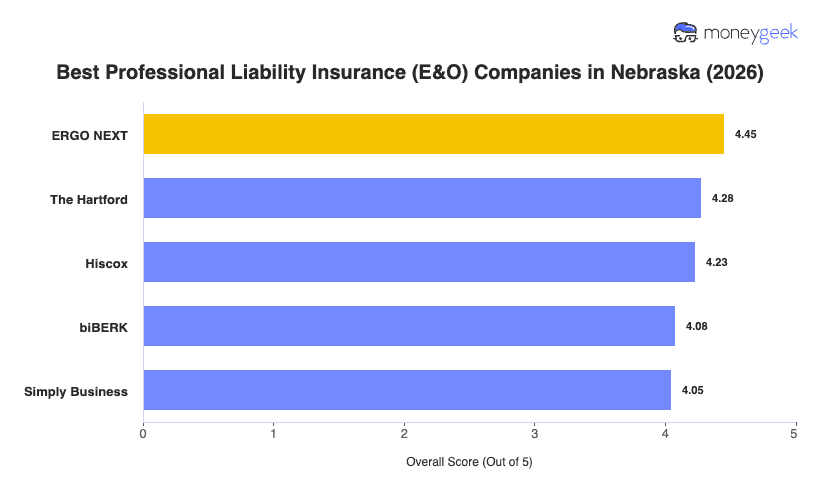

Our analysis of Nebraska professional liability insurers found three providers that consistently outperformed the field on affordability, customer experience and coverage quality.

- ERGO NEXT: A fast, digital-first buying experience and strong rates across a wide range of Nebraska industries earned ERGO NEXT the top spot. The insurer ranks first in Nebraska for cleaning services, health care, fitness, marketing, tech, childcare, pet care, construction and several other categories. Consulting firms, educators and financial services businesses will find better overall value elsewhere, as ERGO NEXT ranks seventh in those industries in Nebraska.

- The Hartford: With more than 200 years in the industry, The Hartford offers underwriting expertise and claims support that generalist insurers can't match. It ranks first or second in Nebraska for consulting, financial services, education and tech businesses, thanks to deep profession-specific expertise. The Hartford ranks ninth in Nebraska for health care and other professional services, so businesses in those fields should compare additional quotes.

- Hiscox: Built for small businesses and solo practitioners, Hiscox covers virtually every industry that needs professional liability insurance and ranks first in Nebraska for real estate professionals. Its digital quoting process lets Nebraska businesses get covered in minutes, and its strong nonprofit and childcare scores make it a reliable option across the state's service economy.

Ranked providers represent strong fits for most Nebraska businesses, but no single list captures every situation. Comparing business insurance options and pulling quotes directly from carriers gives you the clearest picture of what you'll actually pay.