The average cost of tech business insurance is $77 a month, or $924 a year, based on MoneyGeek's analysis across six common coverage types, eight sub-industries, 50 states and Washington, D.C., for businesses with one to four employees at $1 million per occurrence limits.

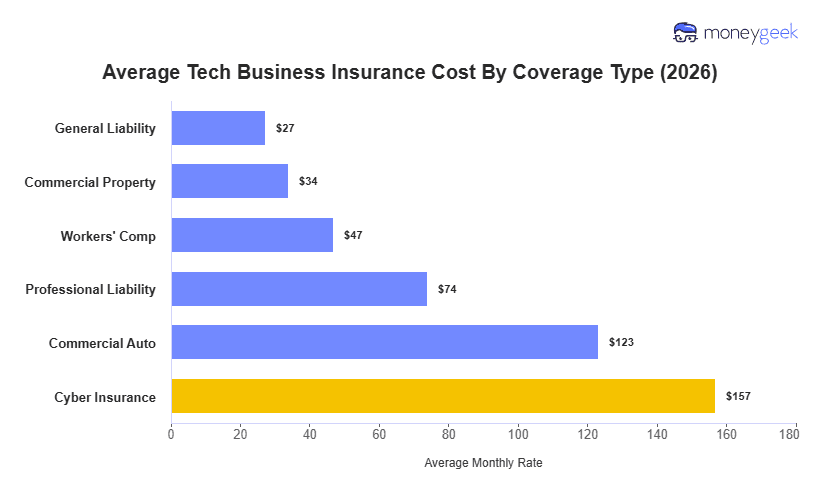

General liability costs around $27 a month, the lowest of the six coverage types, because most tech businesses have limited exposure to third-party physical claims. Cyber insurance averages $157 a month, more than five times the GL figure. That gap comes from the data exposure, software liability and system access risks that insurers price heavily for tech operations. The figures below are benchmarks. Actual premiums vary by business profile.