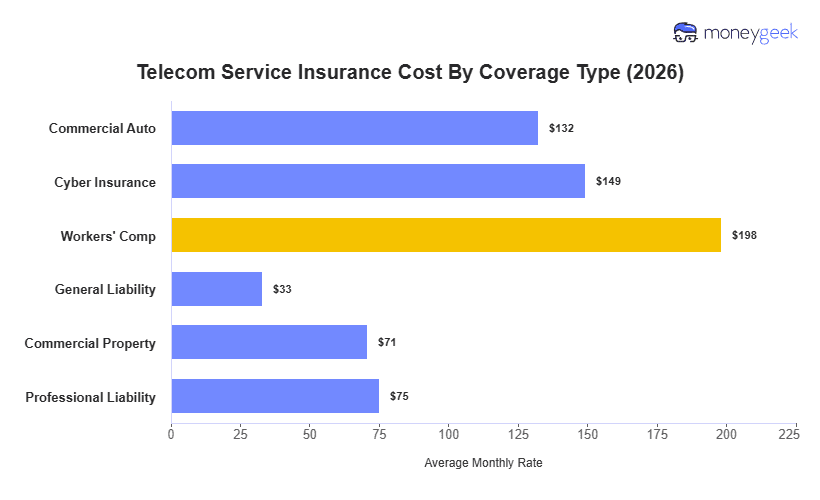

Telecom service business insurance covers the claims, losses and liability that come with running fiber, pulling cable and managing client networks. Exposures range from physical damage on a job site to a dispute over whether an installation met spec.

Your business faces consistent exposure from:

- A drill through a water line or live conduit while running cable in a finished commercial space

- Fusion splicer, OTDR unit or cable tester stolen from a job site vehicle overnight

- A technician injured on a rooftop or cell tower during antenna installation

- A client claiming a network installation didn't perform to spec

The right mix of tech business insurance depends on which type of risk is most likely to follow you. A sole technician doing residential cable drops faces mostly physical job site exposure: property damage, vehicle accidents and equipment loss. A firm managing enterprise networks or certifying cabling runs adds a second layer: claims rooted in whether the work performed as promised, which general liability doesn't cover.