ERGO NEXT is the best workers' comp provider in Oregon, combining the state's lowest monthly rate with strong customer experience. Coverdash and Simply Business follow as competitive runner-up options for Oregon small businesses.

Best Workers' Comp Insurance in Oregon (2026)

With rates starting at $11 per month, ERGO NEXT, Coverdash and Simply Business offer the cheapest and best workers' comp insurance in Oregon.

Get matched to top Oregon workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 27, 2026

Advertising & Editorial Disclosure

ERGO NEXT is Oregon's cheapest workers' comp provider at $76 a month and is also the best workers' comp insurance overall. Coverdash and Simply Business round out the top three most affordable options.

- ERGO NEXT: $76 a month

- Coverdash: $95 a month

- Simply Business: $98 a month

- Thimble: $99 a month

- Hiscox: $104 a month

Oregon requires most employers with one or more employees to carry workers' comp insurance, though sole proprietors and certain corporate officers may opt out. Non-compliance results in Class C felony charges, fines up to $125,000 and potential closure orders from state authorities.

Oregon's average workers' comp insurance cost is $104 per month per employee. Costs vary widely by industry. Beauty, Body & Wellness Services is the cheapest at an average of $15 a month, while Transportation & Logistics is the most expensive at $316 a month. Provider rates within each industry may be lower than the industry average.

Oregon operates as a competitive market, meaning employers can purchase workers' comp insurance from private carriers or from SAIF Corporation, the state's public workers' comp insurer. Employers who cannot secure coverage in the private market have access to the assigned risk pool as a fallback option.

Workers' compensation in Oregon covers:

- Medical expenses for workplace injuries and occupational illnesses

- Wage replacement benefits during recovery periods

- Permanent disability payments for lasting impairments

- Death benefits for families of workers killed in job-related accidents

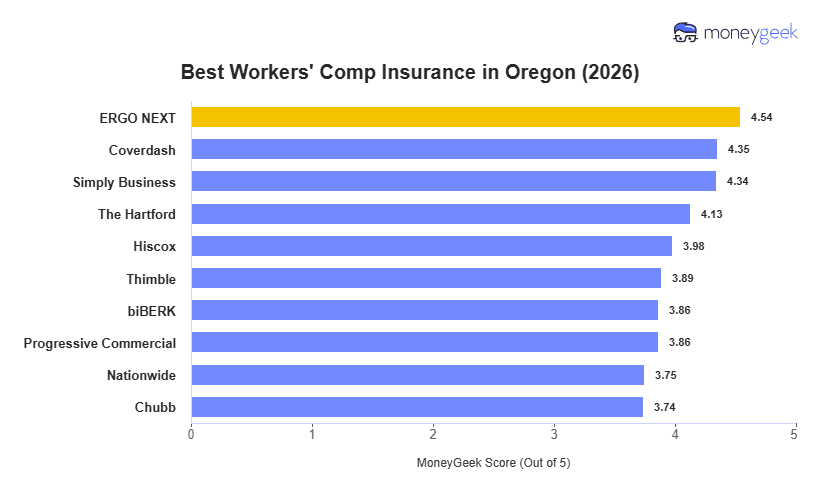

Best Workers' Comp Insurance Companies in Oregon

| ERGO NEXT | 4.54 | $76 | 1 | 6 |

| Coverdash | 4.35 | $95 | 5 | 1 |

| Simply Business | 4.34 | $98 | 2 | 2 |

| The Hartford | 4.13 | $109 | 3 | 3 |

| Hiscox | 3.98 | $104 | 6 | 10 |

| Thimble | 3.89 | $99 | 8 | 9 |

| biBERK | 3.86 | $106 | 8 | 8 |

| Progressive Commercial | 3.86 | $106 | 8 | 7 |

| Nationwide | 3.75 | $115 | 6 | 5 |

| Chubb | 3.74 | $130 | 3 | 4 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

ERGO NEXT

Best Workers' Comp Insurance in Oregon

MoneyGeek Rating

4.5/ 5

4.8/5Affordability

4.4/5Customer Experience

3.6/5Coverage Options

Average Monthly Cost

$76Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

Coverdash

Best Oregon Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.3/ 5

4.5/5Affordability

4/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost

$95Claims Processing Score

4/5Policy Management Score

4/5Buying Process Score

4/5

LEARN MORE ABOUT OREGON BUSINESS INSURANCE

Cheapest Workers' Comp Insurance Companies in Oregon

ERGO NEXT is Oregon's cheapest workers' comp provider at $76 a month ($912/year), 27% below the state average of $104 a month. Coverdash follows at $95 a month and Simply Business at $98 a month.

The most interesting finding in our analysis is the $54 a month gap between ERGO NEXT and Chubb ($130), which translates to $648/year per employee in potential savings. For a business with four employees, that adds up to a difference of $2,592 annually, highlighting the importance of comparison shopping.

| ERGO NEXT | $76 | $912 |

| Coverdash | $95 | $1,140 |

| Simply Business | $98 | $1,176 |

| Thimble | $99 | $1,188 |

| Hiscox | $104 | $1,248 |

| biBERK | $106 | $1,272 |

| Progressive Commercial | $106 | $1,272 |

| The Hartford | $109 | $1,308 |

| Nationwide | $115 | $1,380 |

| Chubb | $130 | $1,560 |

Cheapest Workers' Comp Insurance in Oregon by Industry

ERGO NEXT has the lowest rates in the state for 20 of the 25 industries we tracked, including every high-risk category. The Hartford wins the remaining five.

That split isn't random. The Hartford's five cheapest rates cluster in industries with credentialed workforces and low physical-injury exposure. ERGO NEXT leads across every industry with hands-on work, from Cleaning Services ($88 a month) to Construction ($180 a month) and Transportation & Logistics ($231 a month).

| Beauty, Body & Wellness Services | ERGO NEXT | $11 | $132 |

| Financial Services | The Hartford | $11 | $132 |

| Marketing & Communications | ERGO NEXT | $12 | $144 |

| Consulting Services | The Hartford | $16 | $192 |

| Real Estate & Property Services | The Hartford | $17 | $204 |

| Other Professional Services | ERGO NEXT | $19 | $228 |

| Childcare Services | ERGO NEXT | $30 | $360 |

| Food & Beverage | ERGO NEXT | $32 | $384 |

| Tech/IT | The Hartford | $32 | $384 |

| Hospitality, Travel & Tourism | ERGO NEXT | $36 | $432 |

| Healthcare & Medical | The Hartford | $41 | $492 |

| Retail & Product Rental | ERGO NEXT | $42 | $504 |

| Nonprofit & Associations | ERGO NEXT | $47 | $564 |

| Pet Care Services | ERGO NEXT | $48 | $576 |

| Education | ERGO NEXT | $52 | $624 |

| Fitness Services | ERGO NEXT | $52 | $624 |

| Repair & Maintenance | ERGO NEXT | $55 | $660 |

| Arts, Media & Entertainment | ERGO NEXT | $74 | $888 |

| Recreation & Sports | ERGO NEXT | $85 | $1,020 |

| Cleaning Services | ERGO NEXT | $88 | $1,056 |

| Manufacturing | ERGO NEXT | $113 | $1,356 |

| Agriculture & Natural Resources | ERGO NEXT | $125 | $1,500 |

| Wholesale & Distribution | ERGO NEXT | $149 | $1,788 |

| Construction & Contracting | ERGO NEXT | $180 | $2,160 |

| Transportation & Logistics | ERGO NEXT | $231 | $2,772 |

How Much Is Workers' Comp Insurance in Oregon?

The average monthly rate for workers' comp insurance in Oregon is $104 per employee, above the national average of $74. Costs vary widely by industry in our analysis. Beauty, Body and Wellness Services is the cheapest at an average of $15 a month, while Transportation and Logistics is the most expensive at $316 a month.

A few patterns in our data are worth calling out. Tech and IT ($44 a month) lands in the same tier as Hospitality, Travel and Tourism ($44 a month), which surprises most business owners who assume their desk-based workforce is automatically considered low-risk. Oregon's workers' comp system rates industries based on historical claim frequency and severity, so a cleaning crew or construction crew costs more to insure than a marketing team.

| Beauty, Body & Wellness Services | $15 | $180 |

| Financial Services | $15 | $180 |

| Marketing & Communications | $16 | $192 |

| Consulting Services | $21 | $252 |

| Real Estate & Property Services | $22 | $264 |

| Other Professional Services | $24 | $288 |

| Childcare Services | $38 | $456 |

| Food & Beverage | $42 | $504 |

| Hospitality, Travel & Tourism | $44 | $528 |

| Tech/IT | $44 | $528 |

| Healthcare & Medical | $52 | $624 |

| Retail & Product Rental | $56 | $672 |

| Nonprofit & Associations | $59 | $708 |

| Pet Care Services | $66 | $792 |

| Fitness Services | $67 | $804 |

| Education | $68 | $816 |

| Repair & Maintenance | $76 | $912 |

| Arts, Media & Entertainment | $96 | $1,152 |

| Recreation & Sports | $119 | $1,428 |

| Cleaning Services | $124 | $1,488 |

| Manufacturing | $147 | $1,764 |

| Agriculture & Natural Resources | $171 | $2,052 |

| Wholesale & Distribution | $188 | $2,256 |

| Construction & Contracting | $290 | $3,480 |

| Transportation & Logistics | $316 | $3,792 |

Oregon Workers' Comp Insurance Cost Factors

Oregon workers' comp rates are set using class codes administered by the Workers' Compensation Division of the Department of Consumer and Business Services (DCBS), which serves as the state's rating bureau. SAIF Corporation operates alongside private carriers in Oregon's competitive market, which produces real pricing variation across providers.

How Much Workers' Comp Insurance Do I Need in Oregon?

Oregon law requires workers' compensation insurance for all employers with one or more employees. The required workers' compensation coverage must provide full medical benefits with no dollar limits, temporary disability payments of two-thirds of average weekly wages, permanent disability compensation based on injury severity, and death benefits for families.

Failing to carry coverage results in penalties of $1,000 or twice the premium owed (whichever is greater), plus $250 daily for continued noncompliance. You're also personally liable for all benefits injured workers would have received, potentially exceeding $100,000 per claim.

Oregon Workers' Comp Insurance Exemptions

While you're often required to have coverage in Oregon, some business categories are exempt from workers' comp requirements:

- Sole proprietors: You don't need coverage for yourself as a sole proprietor, but you must meet Oregon's independent contractor criteria if you work under contract for other businesses.

- Business partners: Partners skip coverage requirements unless you're in construction, which caps exemptions at two partners. Family-run partnerships where everyone is related (parents, spouses, siblings, children, in-laws, or grandchildren) can exempt all partners.

- LLC members: Most LLC members don't need coverage for themselves and follow corporate officer exemption rules based on ownership percentage and board participation.

- Corporate officers: You can opt out of coverage when you serve on your company's board and own at least 10% of the stock. Construction corporations limit this to two officers unless your family owns and operates the business.

- Domestic and household workers: Workers you hire for household services at your private home are exempt, including home health aides, gardeners, and people doing maintenance, repairs or remodeling at your residence.

- Casual labor: Workers stay exempt when your total labor costs remain under $1,000 in any 30-day period and the work falls outside your regular business operations.

- Volunteer and unpaid workers: Voluntary carpoolers (groups of 15 or fewer commuting together), ACTION program volunteers, and municipal volunteers your city hasn't elected to cover skip coverage requirements.

- Media and sports workers: Newspaper carriers meeting Oregon's delivery requirements and soccer referees working individual matches on a per-game basis don't need coverage.

- Amateur athletes and officials: Olympic-level amateur athletes who receive only lodging and basic expenses are exempt, as are certified amateur sports officials whose certifying organizations provide liability insurance.

- Religious and charitable workers: People working primarily for room and board from religious, charitable, or relief organizations don't require coverage.

- Self-employed licensed contractors: Landscape and construction business owners with active Oregon licenses and substantial ownership automatically qualify for exemption.

- Real estate professionals: Certain real estate workers meeting Oregon's specific criteria under ORS 656.037 qualify for exemption.

- Independent contractors and out-of-state workers: Workers you bring into Oregon temporarily don't need Oregon coverage if your home state policy covers them, your state offers reciprocal coverage for Oregon employers, and you don't hire Oregon residents.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal workers' comp programs, including the Federal Employees' Compensation Act (FECA), the Federal Employers' Liability Act (FELA), and the Longshore and Harbor Workers' Compensation Act, apply to specific employee categories regardless of Oregon state requirements. Oregon employers with workers in maritime, railroad, or federal government roles should confirm which program governs their workforce before purchasing a state policy.

How to Get the Best Workers' Comp Insurance in Oregon

Getting the right workers' comp coverage in Oregon requires more than finding the lowest rate. Follow these steps to secure compliant, cost-effective coverage for your Oregon business. See additional guidance at how to get workers' compensation insurance.

- 1

Confirm Oregon Coverage Requirements

Oregon requires workers' comp coverage before your first employee begins work. Contact the Workers' Compensation Division of the Department of Consumer and Business Services (DCBS) to confirm your obligations, including any exemptions that apply to your ownership structure or workforce type.

- 2

Identify Your Class Codes Accurately

The state of Oregon uses class codes administered by the Workers' Compensation Division of DCBS to set base rates. Each employee role carries its own code, and premiums are calculated by applying that rate to payroll. Accurate classification prevents audit adjustments at renewal and retroactive premium charges.

- 3

Document Payroll, Employee Count and Claims History

Pull current payroll figures, total employee count and prior workers' comp claims before requesting quotes. Oregon insurers use this information to calculate your experience modification rate (EMR), which adjusts your base premium up or down based on your claims history relative to industry peers.

- 4

Request Quotes From Multiple Licensed Oregon Carriers

Select three sources to get quotes from, including private carriers and SAIF Corporation, Oregon's state fund insurer. SAIF must quote any eligible Oregon employer and can't decline coverage based on industry or claims history.

- 5

Compare Total Value, Not Just Monthly Rate

Check each quote for coverage limits, employers' liability limits, audit provisions and claims support quality. A lower monthly rate with poor claims handling can end up costing more over time. Use MoneyGeek's CX scores as a starting point for evaluating service quality alongside price.

- 6

Complete Purchase and Establish Payroll and Audit Reporting

Bind coverage before your employees begin work. Set up payroll reporting in accordance with your policy. Most Oregon workers' comp policies are auditable, meaning your final premium is adjusted at year-end based on actual payroll. Accurate mid-year reporting reduces the risk of a large audit balance due at renewal.

- 7

Review at Annual Renewal

Oregon workers' comp premiums shift at renewal based on changes to your payroll, class codes, EMR and state rate filings. Pull your renewal quote at least 30 days before expiration. Re-quote with competing carriers if rates have increased and confirm your class codes still reflect your current workforce.

Bottom Line

ERGO NEXT, Coverdash and Simply Business are Oregon's strongest workers' comp options for most small businesses. ERGO NEXT leads on both price and customer experience, while Coverdash and Simply Business offer competitive alternatives for employers who want multiple quotes before committing. Your best fit depends on your industry, claims history and how much weight you place on verified service quality versus upfront cost.

Next Steps

Oregon workers' comp rates vary by industry, employee count and claims history. Use the resources below to sharpen your estimate and connect with licensed Oregon carriers.

Oregon Workers' Compensation Insurance FAQ

Oregon workers' comp covers employees based in Oregon. Coverage for remote workers in other states depends on where the employee primarily works. Employers with remote workers outside Oregon should notify their carrier to confirm if the policy extends coverage to the employee's home state, or get a separate policy in that state.

Oregon insurers apply an experience modification rate (EMR) to adjust your base premium based on your claims history relative to industry peers. An EMR below 1.0 reduces your premium. An EMR above 1.0 increases it. Oregon employers lower their EMR over time by cutting claims frequency and severity through workplace safety programs.

Sole proprietors and certain corporate officers can apply to exempt themselves from workers' comp coverage in Oregon under conditions set by the Workers' Compensation Division of DCBS. Partners in a partnership aren't considered employees under Oregon law. Employers considering an opt-out should confirm current eligibility criteria with DCBS before removing themselves from a policy.

Workers' comp covers an injured employee's medical costs and wage replacement without regard to fault. Employer's liability coverage, typically included in Part Two of a workers' comp policy, covers the employer against lawsuits from employees who claim negligence outside the workers' comp system. Oregon employers should confirm that their policy includes both components.

Workers' comp claims in Oregon generally affect an employer's experience modification rate for three years, excluding the most recent policy year. A single large claim can elevate your EMR and increase premiums across multiple renewal cycles. Oregon employers should report all workplace injuries promptly and work with their carrier to manage claim costs from the point of first notice.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Oregon using small business profiles with one to four employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.

Sources

- Insurance Journal. "Oregon Workers' Comp Pure Premium Rate to Drop 3.2%.." Accessed July 13, 2026.

- Oregon Department of Consumer and Business Services. "Workers' Compensation Comparison Across the States." Accessed July 13, 2026.

- Oregon Department of Consumer and Business Services. "Workers' Compensation Pure Premium Rate to Drop for 12th-Straight Year." Accessed July 13, 2026.

- Oregon Health Policy Board. "What is SAIF." Accessed July 13, 2026.

- Oregon Public Law. "ORS 656.027 – Who Are Subject Workers." Accessed July 13, 2026.

- SAIF Corporation. "Premium and Rate Overview." Accessed July 13, 2026.