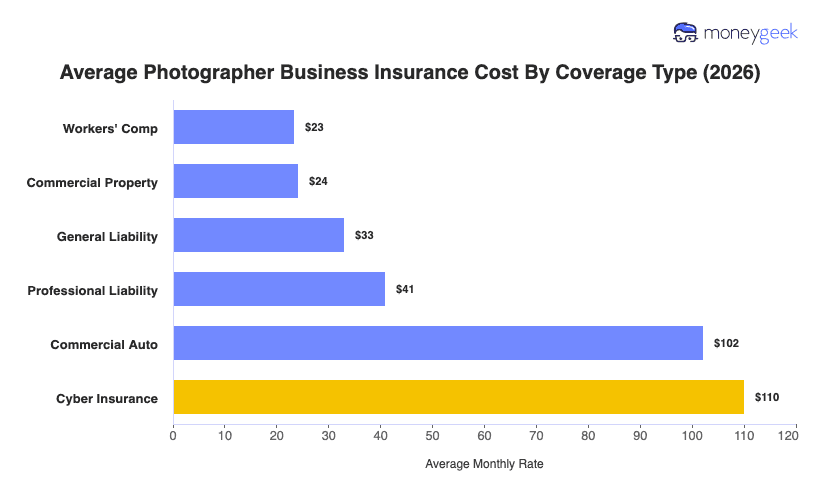

On average, photographer business insurance costs between $227 for a starting bundle to $1,206 for expanded operations, depending on the bundle that suits your operations. These figures were modeled for photography businesses with one to four employees, so your actual rate could vary. But business size isn't the only factor that insurers consider. A photographer who travels to different locations for shoots needs different coverages in his policy mix than if you had your own studio.

Use the table below to see which bundle matches your business's services: