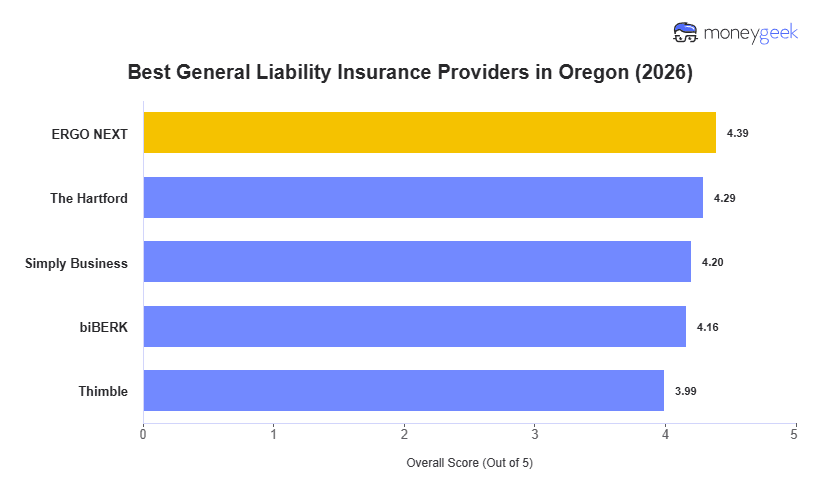

Every Oregon business has different coverage needs, so we reviewed 10 major general liability insurers across 25 industries to find the strongest performers. The five companies listed below offer the best and most affordable coverage in the state, based on quotes at $1 million per occurrence/$2 million aggregate limits:

- ERGO NEXT: Best Overall, Best for Higher-Risk and Hands-On Industries

- The Hartford: Best Cheap General Liability Insurance

- Simply Business: Best for Varied Coverage Options

- biBERK: Best for Active Service Businesses

- Thimble: Best for Seasonal and Project-Based Businesses

Whether you're a fishing guide on the Columbia River or a contractor rebuilding after wildfire season, the table below shows how each provider's rates and rankings compare. Use it to find coverage that fits your operations and budget, then review individual provider details further down the page.