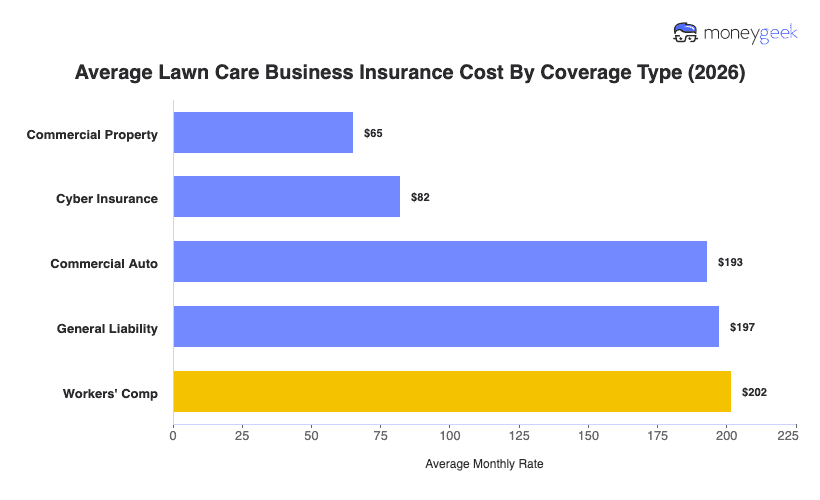

Lawn care business insurance costs range from an average of $390 per month for a minimum starting bundle to $931 for a full-service one, depending on which one fits your operations. Your total cost increases as you include more coverages in your policy mix, whether it's workers' comp when you hire employees or pesticide/herbicide applicator coverage when you start offering lawn treatment services.

We used national averages, so use them to understand the relative cost of each bundle rather than as exact quotes. Use the table below to compare the different bundles and see which one fits your lawn care business: