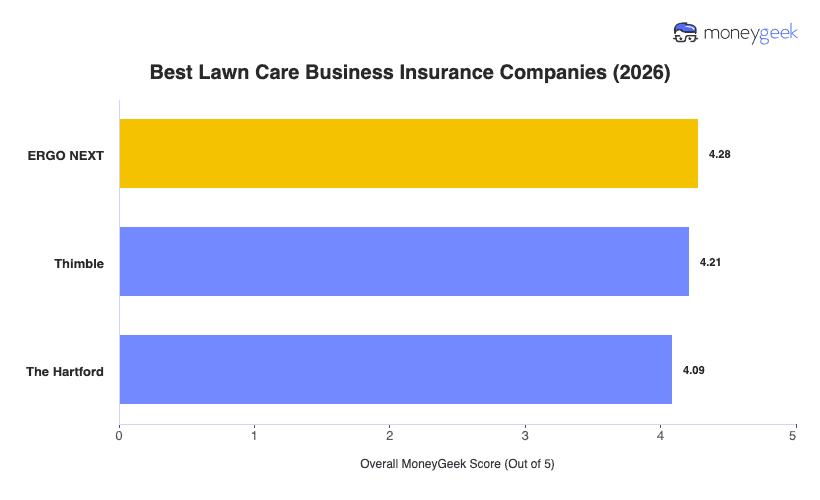

Based on my analysis of seven major carriers for lawn care business insurance, I'd recommend ERGO NEXT for most companies. But having the highest overall score in our study doesn't mean it's the best choice for everyone. If you’re starting out or doing lawn care part time, a traditional year-round policy may not fit your work schedule. If you manage a larger crew, serve more commercial clients or need coverage for vehicles, trailers and stored equipment, an insurer with broader coverage options may be a better match.

I've put together a table to help choose which providers suit your business: