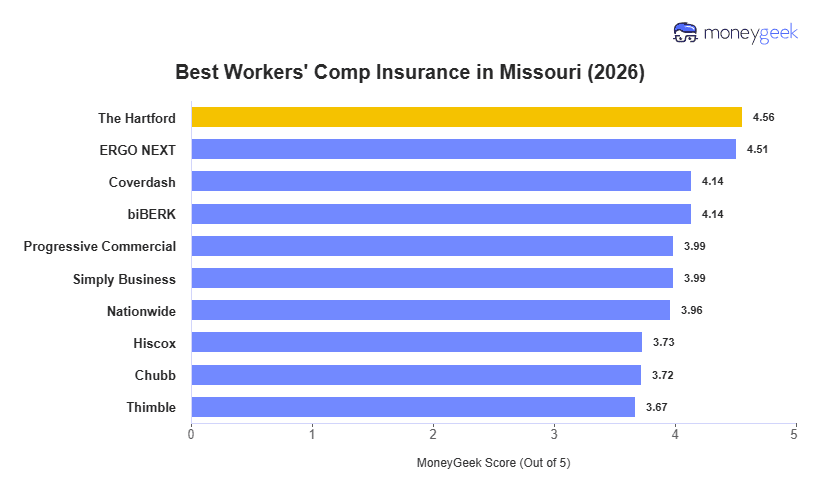

The Hartford leads Missouri's workers' comp rankings with the highest MoneyGeek score, driven by the state's top affordability rank and strong claims performance. ERGO NEXT ranks second at $66 a month, $2 cheaper than The Hartford's $68 a month average, and holds the highest customer experience score in the state.

The $54 spread between ERGO NEXT ($66 a month) and the most expensive ranked provider, Chubb ($120 a month), is meaningful for Missouri's large professional and service employer base. Construction and transportation class codes compress that spread across allcarriers.