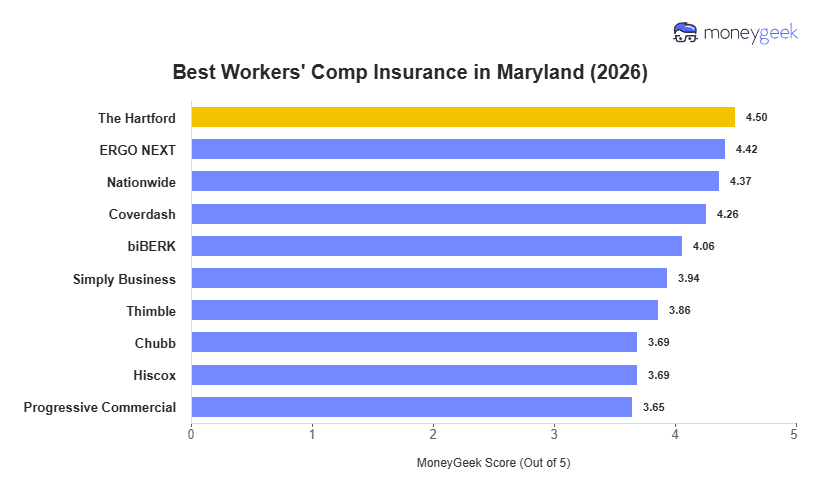

The Hartford leads Maryland's workers' comp insurance market with the state's highest MoneyGeek score. All three leading providers, The Hartford, NEXT, and Nationwide, fall within the $95 to $96 per month, making service quality and industry-specific rate position the main differentiators.

The broader Maryland market spans from Nationwide at $95 per month to Chubb at $163 per month, a $68 monthly spread. Professional-sector employers in financial services, tech, and marketing gain the most from comparing providers at the lower end of that range. Construction and transportation class codes narrow the pricing gap between providers.