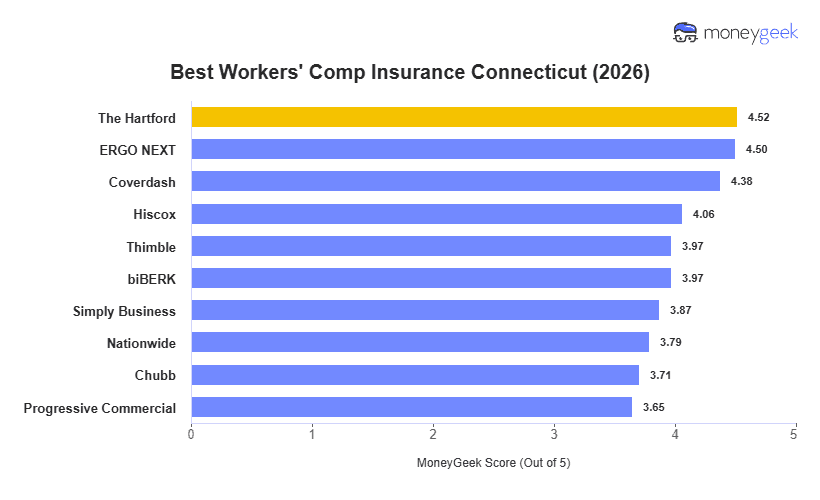

The Hartford is the best workers' comp insurance provider in Connecticut with the top MoneyGeek score, combining the state's second-lowest average rate with the strongest claims handling in the market. ERGO NEXT ranks second with the lowest monthly average at $148.

The difference between ERGO NEXT ($148 a month) and Progressive Commercial ($232 a month) is $84. In Connecticut's high-wage market, that gap multiplies quickly for employers with multi-person payrolls. That advantage reverses in financial services and professional services. The Hartford posts lower per-industry rates in those categories.