The Hartford has the best workers' comp insurance in Texas with competitive rates, strong customer support and comprehensive coverage options. ERGO NEXT and Thimble are reliable alternatives for small business owners.

Best Workers' Comp Insurance in Texas (2026)

With rates as low as $8 monthly per employee, The Hartford, ERGO NEXT and Thimble have the best workers' comp insurance in Texas.

Get matched to top Texas workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 30, 2026

Advertising & Editorial Disclosure

Best Texas Workers' Comp Insurance: Fast Answers

The Hartford and ERGO NEXT tie as the cheapest workers' comp provider in Texas at $59 a month per employee, while The Hartford is our top pick among best workers' comp insurance providers. Here are the five most affordable options in the state:

- The Hartford: $59 a month

- ERGO NEXT: $59 a month

- Thimble: $65 a month

- biBerk: $70 a month

- Coverdash: $75 a month

Texas is the only state where workers' comp insurance remains optional for most private employers, but employers who skip coverage lose legal protections against workplace injury lawsuits and face unlimited liability. Government entities and construction companies working on public projects must maintain coverage.

The cost of workers' compensation insurance in Texas is about $76 per employee monthly for small businesses. Your costs depend on your industry and payroll size. Low-risk industries, like Beauty, Body & Wellness Services, pay an average of $13 per month per employee, while high-risk industries, like Construction & Contracting average $211.

You can get workers' comp coverage in Texas by:

- Purchasing policies from private insurance companies licensed to operate in Texas

- Buying coverage through the Texas Mutual Insurance Company, a policyholder-owned carrier

- Qualifying for self-insurance status if your business meets the state's strict financial requirements

Many business owners compare quotes online or through brokers to get the best rate and compliance support.

Workers' compensation in Texas covers:

- Medical expenses for workplace injuries and occupational illnesses

- Temporary income benefits replacing two-thirds of lost wages during recovery

- Impairment income benefits for permanent disabilities based on medical assessments

- Death benefits for surviving family members of workers killed in workplace accidents

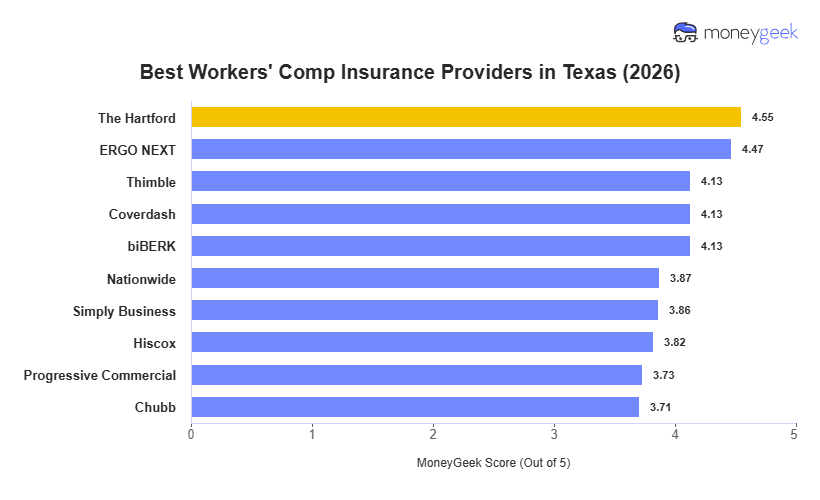

Best Workers' Comp Insurance Companies in Texas

| The Hartford | 4.55 | $59 | 2 | 3 |

| ERGO NEXT | 4.47 | $59 | 1 | 6 |

| Thimble | 4.13 | $65 | 8 | 9 |

| Coverdash | 4.13 | $75 | 7 | 1 |

| biBERK | 4.13 | $70 | 8 | 8 |

| Nationwide | 3.87 | $80 | 5 | 5 |

| Simply Business | 3.86 | $85 | 4 | 2 |

| Hiscox | 3.82 | $83 | 5 | 10 |

| Progressive Commercial | 3.73 | $84 | 8 | 7 |

| Chubb | 3.71 | $102 | 2 | 4 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

The Hartford

Best Workers' Comp Insurance in Texas

MoneyGeek Rating

4.5/ 5

4.7/5Affordability Score

4.3/5Customer Experience Score

4.1/5Coverage Score

Average Monthly Cost

$59Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

ERGO NEXT

Best Texas Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.5/ 5

4.7/5Affordability Score

4.3/5Customer Experience Score

3.8/5Coverage Score

Average Monthly Cost

$59Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

LEARN MORE ABOUT TEXAS BUSINESS INSURANCE

Cheapest Workers' Comp Insurance Companies in Texas

The Hartford offers the cheapest workers’ compensation insurance in Texas at about $59 per employee monthly ($708 annually), roughly 8% below the state average of $64 per month. ERGO NEXT matches The Hartford at $59 monthly, while Thimble ranks third at $65.

The price difference between lower-cost providers and higher-priced insurers can be great. For example, Chubb averages about $102 monthly per employee, or roughly $516 more per year than The Hartford. Savings matter most for small businesses with tighter payroll budgets, though pricing differences between providers often narrow in higher-risk industries where underwriting plays a larger role in final premiums.

| The Hartford | $59 | $708 |

| ERGO NEXT | $59 | $708 |

| Thimble | $65 | $780 |

| biBERK | $70 | $840 |

| Coverdash | $75 | $900 |

| Nationwide | $80 | $960 |

| Hiscox | $83 | $996 |

| Progressive Commercial | $84 | $1,008 |

| Simply Business | $85 | $1,020 |

| Chubb | $102 | $1,224 |

Cheapest Workers' Comp in Texas by Industry

The Hartford and ERGO NEXT provide the lowest workers’ compensation rates in 24 of the 25 Texas industries we analyzed. ERGO NEXT leads on price in 14 industries, while The Hartford offers the cheapest rates in 10. biBerk ranks lowest for childcare businesses at about $22 monthly per employee.

The Hartford is generally the more affordable option for lower-risk, office-based industries, including financial services ($8 a month), consulting ($11), real estate ($12) and tech/IT ($23). ERGO NEXT has lower pricing in industries with greater physical labor or workplace exposure, like cleaning services ($66), construction ($138) and transportation ($174).

| Financial Services | The Hartford | $8 | $96 |

| Beauty, Body & Wellness Services | ERGO NEXT | $9 | $108 |

| Marketing & Communications | ERGO NEXT | $9 | $108 |

| Consulting Services | The Hartford | $11 | $132 |

| Real Estate & Property Services | The Hartford | $12 | $144 |

| Other Professional Services | The Hartford | $15 | $180 |

| Childcare Services | biBERK | $22 | $264 |

| Tech/IT | The Hartford | $23 | $276 |

| Food & Beverage | ERGO NEXT | $24 | $288 |

| Hospitality, Travel & Tourism | The Hartford | $24 | $288 |

| Healthcare & Medical | The Hartford | $26 | $312 |

| Retail & Product Rental | The Hartford | $30 | $360 |

| Nonprofit & Associations | The Hartford | $34 | $408 |

| Pet Care Services | ERGO NEXT | $36 | $432 |

| Education | ERGO NEXT | $38 | $456 |

| Fitness Services | ERGO NEXT | $41 | $492 |

| Repair & Maintenance | ERGO NEXT | $43 | $516 |

| Arts, Media & Entertainment | ERGO NEXT | $56 | $672 |

| Recreation & Sports | ERGO NEXT | $65 | $780 |

| Cleaning Services | ERGO NEXT | $66 | $792 |

| Manufacturing | The Hartford | $86 | $1,032 |

| Agriculture & Natural Resources | ERGO NEXT | $95 | $1,140 |

| Wholesale & Distribution | ERGO NEXT | $111 | $1,332 |

| Construction & Contracting | ERGO NEXT | $138 | $1,656 |

| Transportation & Logistics | ERGO NEXT | $174 | $2,088 |

How Much Is Workers' Comp Insurance in Texas?

Texas workers’ compensation rates average about $76 monthly per employee, slightly above the national average of $74. But costs vary widely by industry. The gap between the cheapest and most expensive industries in our analysis reaches roughly $213 per employee monthly, with cleaning service businesses paying about seven times more than financial services firms for the same required coverage.

Rates rise steeply in industries involving physical labor and higher workplace risk. Office-based and client-facing businesses fall between $13 and $50 monthly per employee, while industries such as cleaning, manufacturing, agriculture and construction see much higher premiums. The two most expensive industries in our analysis, construction and transporation, both exceed $200 monthly per employee.

| Beauty, Body & Wellness Services | $13 | $156 |

| Financial Services | $13 | $156 |

| Marketing & Communications | $13 | $156 |

| Consulting Services | $16 | $192 |

| Real Estate & Property Services | $18 | $216 |

| Other Professional Services | $20 | $240 |

| Childcare Services | $28 | $336 |

| Food & Beverage | $30 | $360 |

| Hospitality, Travel & Tourism | $33 | $396 |

| Tech/IT | $34 | $408 |

| Healthcare & Medical | $39 | $468 |

| Retail & Product Rental | $41 | $492 |

| Nonprofit & Associations | $44 | $528 |

| Education | $48 | $576 |

| Pet Care Services | $48 | $576 |

| Fitness Services | $50 | $600 |

| Repair & Maintenance | $56 | $672 |

| Arts, Media & Entertainment | $71 | $852 |

| Recreation & Sports | $88 | $1,056 |

| Cleaning Services | $90 | $1,080 |

| Manufacturing | $108 | $1,296 |

| Agriculture & Natural Resources | $125 | $1,500 |

| Wholesale & Distribution | $138 | $1,656 |

| Construction & Contracting | $211 | $2,532 |

| Transportation & Logistics | $226 | $2,712 |

Texas Workers' Comp Insurance Cost Factors

Texas workers' comp rates are set in a private competitive market regulated by the Texas Department of Insurance, Division of Workers' Compensation. NCCI class codes are the primary rating tool, and the state's non-subscriber option creates a unique cost dynamic not found in other states.

How Much Workers' Comp Insurance Do I Need in Texas?

Texas law doesn't require most private employers to carry workers' comp. You decide whether to provide it. The exception is if you contract with government entities, you're required to have workers' compensation insurance for employees working those projects. When you buy coverage, your policy covers all eligible employees based on your payroll and industry classification, including full medical care, two-thirds of wages during disability and permanent injury benefits.

Texas non-subscribers lose legal protections that workers' comp coverage provides. Injured employees can sue non-subscribing employers for medical bills, lost wages and damages. Non-subscribers must file annual reports with the Texas Department of Insurance and notify employees of their non-coverage status.

Texas Workers' Comp Insurance Exemptions

These business categories in Texas are exempt from workers' comp requirements:

- Sole proprietors and partners: Sole proprietors and partners can exclude themselves from coverage, whether they run their business alone or with partners, though a policy covers medical expenses if the owner is injured on the job.

- Self-employed professionals: Working without employees makes a business owner automatically exempt, but many self-employed Texans buy coverage to avoid out-of-pocket medical bills.

- LLC members and corporate officers: Texas includes LLC members and corporate officers in workers' comp by default, but they can opt out.

- Independent contractors: True independent contractors who control their own schedule, handle their own expenses and work with multiple clients rather than functioning like an employee are exempt.

- Domestic and agricultural workers: Household employees and farm workers fall outside workers' comp requirements, even when the employer carries a policy.

- Casual and temporary workers: Short-term hires and seasonal help generally aren't covered under workers' comp rules.

- Volunteers: Volunteers are exempt from coverage requirements, though employers can cover volunteer firefighters and emergency responders.

- Certain real estate agents: Agents who meet specific Texas criteria don't need workers' comp coverage.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal programs including the Federal Employees' Compensation Act (FECA), the Federal Employers' Liability Act (FELA) and the Longshore and Harbor Workers' Compensation Act govern specific worker categories regardless of Texas state rules. Texas employers with maritime workers, railroad employees or federal contractors must comply with the applicable federal program, which may provide broader or different benefits than the state system.

How to Get the Best Workers' Comp Insurance in Texas

Follow these steps to find and purchase the right workers' comp coverage for your Texas business.

- 1

Determine Whether Your Texas Business Is Required to Carry Workers' Comp

The state of Texas doesn't require workers' comp for most private employers, but government contractors and certain regulated industries must carry it. But voluntary coverage provides tort immunity: you can't be sued directly by an injured employee for most workplace injuries. Weigh that protection against the premium cost before deciding to opt out.

- 2

Identify Your NCCI Class Codes Accurately

NCCI class codes determine your base rate. Each employee role has a specific code, and the wrong assignment can result in a premium audit or back charge at policy renewal. Review the Texas Department of Insurance, Division of Workers' Compensation guidelines and confirm your classifications with a licensed broker.

- 3

Document Payroll, Employee Count and Claims History

Carriers price workers' comp based on your total payroll, number of employees and loss history. Collect three years of claims data if available. A clean claims record can qualify your business for experience modification rate (EMR) credits that reduce your premium.

- 4

Request Quotes from Multiple Licensed Texas Carriers

Texas's private competitive market means rates vary between carriers for the same class code. Request quotes from at least three to five licensed providers. You can learn how to get workers' compensation insurance and compare options before committing.

- 5

Compare Total Value, Not Just Monthly Rate

The cheapest monthly rate isn't always the best choice. Review each carrier's claims processing score, policy management support and coverage completeness. A provider with a slightly higher premium but faster claims resolution can save your business more in time.

- 6

Complete Purchase and Establish Payroll and Audit Reporting

Complete the application and bind coverage. Set up payroll reporting in accordance with your policy terms. Most workers' comp policies include an annual audit to reconcile estimated payroll against actual figures.

- 7

Review at Annual Renewal

Workers' comp premiums change at renewal based on updated payroll, claims history and carrier rate filings. Review your class codes, EMR and coverage limits each year.

Bottom Line

The Hartford and ERGO NEXT have the best workers' compensation insurance for most Texas employers, tied at $59 a month per employee. Thimble is a competitive third option for businesses that want a digital-first experience at $65 a month. The right choice depends on your industry, claims history, and how much weight you place on claims support versus buying convenience.

Next Steps

After identifying your top Texas workers' comp providers, take these steps to finalize your coverage and keep costs under control.

Texas Workers' Compensation Insurance FAQ

Texas employers who opt out of the workers' comp system lose common-law tort defenses, including the contributory negligence and fellow-servant rule protections. This means an injured employee can sue the employer directly for the full cost of their injury, and the employer has no statutory cap on damages.

A Texas workers' comp policy may not automatically cover employees working in other states. Most policies include an "Other States" endorsement that extends coverage to temporary out-of-state work. Employers with permanent remote employees in other states should confirm coverage with their carrier and may need a separate policy in each state where employees are based.

Your experience modification rate (EMR) is a multiplier applied to your base premium based on your claims history relative to industry peers. An EMR below 1.0 reduces your premium. Above 1.0, it increases your cost. Texas employers with a clean claims record over three or more years can achieve meaningful premium reductions through a favorable EMR.

Yes. Sole proprietors, partners and corporate officers in Texas may elect to include or exclude themselves from workers' comp coverage. Opting out reduces the payroll subject to premium calculation but leaves the owner personally unprotected for work-related injuries. Weigh that decision against the cost of a separate accident or disability policy.

Workers' comp pays statutory benefits directly to injured employees regardless of fault. Employer's liability, Part 2 of a standard workers' comp policy, covers the employer's legal costs if an employee sues outside the workers' comp system. In Texas, non-subscribers have no workers' comp protection and face full employer's liability exposure in every employee injury claim.

Workers' comp claims typically affect your premium record for three policy years through the experience modification rate calculation. A single large claim can raise your EMR and increase premiums across multiple renewal cycles. Reporting claims promptly and working with your carrier on return-to-work programs can limit the long-term premium impact of a single incident.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Texas using small business profiles with one to four employees spanning 408 major industries. The $64 a month Texas state average is derived from this full 408-industry dataset and is not limited to the providers reviewed on this page. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate an overall MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.

Sources

- Insurance Journal. "TDI to Adopt 11.5% Workers' Comp Rate Decrease." Accessed July 20, 2026.

- Texas Department of Insurance. "Employer E-File Online Reporting." Accessed July 20, 2026.

- Texas Department of Insurance. "History of Workers' Compensation in Texas." Accessed July 20, 2026.

- Texas Department of Insurance. "Workers' Compensation Insurance Guide." Accessed July 20, 2026.

- Texas Department of Insurance. "Texas Workers' Compensation Rate Guide." Accessed July 20, 2026.