ERGO NEXT is the top workers' comp provider in Tennessee, combining the lowest available rate with strong customer experience. The Hartford and biBERK are strong runner-up options for employers who prioritize coverage depth and carrier reputation.

Best Workers' Comp Insurance in Tennessee (2026)

With rates as low as $9 per month, ERGO NEXT, The Hartford and biBerk have the best workers' comp insurance in Tennessee.

Get matched to top Tennessee workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 27, 2026

Advertising & Editorial Disclosure

Best Tennessee Workers' Comp Insurance: Fast Answers

What are the best and cheapest workers' comp insurance providers in Tennessee?

ERGO NEXT is Tennessee's cheapest workers' comp provider at $62 a month and is also our top pick for the best workers' comp insurance in the state. The following providers have the lowest monthly rates per employee:

- ERGO NEXT: $62 a month

- biBerk: $72 a month

- Thimble: $74 a month

- Hiscox: $78 a month

- Nationwide: $80 a month

Is workers' comp insurance required in Tennessee?

Tennessee requires workers' comp coverage for most businesses with five or more employees, though construction and mining employers must cover workers starting at one employee. Corporate officers and LLC members may opt out of coverage under certain conditions. Employers who fail to carry required coverage are subject to civil penalties.

How much does workers' comp insurance cost in Tennessee?

The average workers' comp insurance cost in Tennessee is approximately $81 a month per employee. Rates vary widely by industry. Beauty, Body & Wellness Services is the cheapest industry in the state averaging $14 a month, while Transportation & Logistics is the most expensive at $243 a month.

How do you get workers' comp insurance in Tennessee?

You can get workers' comp coverage in Tennessee by:

- Purchasing from licensed private insurance companies operating in the state

- Joining a group self-insurance fund with other qualified employers in your industry

- Becoming individually self-insured if your business meets Tennessee's strict financial requirements

Many business owners compare quotes online or through brokers to get the best rate and compliance support.

What does Tennessee workers' comp insurance cover?

Workers’ compensation in Tennessee covers:

• Medical expenses for workplace injuries and occupational illnesses

• Wage replacement benefits during recovery periods

• Permanent disability compensation for lasting impairments

• Death benefits for families of workers killed in job-related accidents

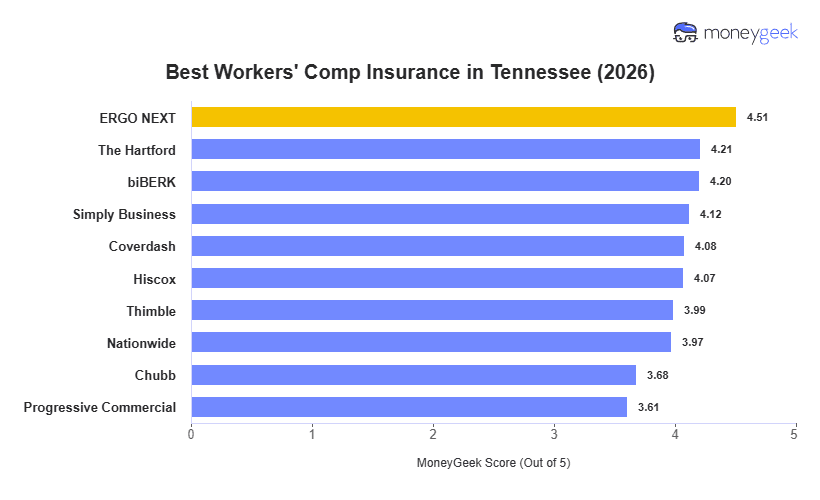

Best Workers' Comp Insurance Companies in Tennessee

| ERGO NEXT | 4.51 | $62 | 1 | 6 |

| The Hartford | 4.21 | $81 | 3 | 3 |

| biBERK | 4.20 | $72 | 8 | 8 |

| Simply Business | 4.12 | $81 | 2 | 2 |

| Coverdash | 4.08 | $81 | 5 | 1 |

| Hiscox | 4.07 | $78 | 6 | 10 |

| Thimble | 3.99 | $74 | 8 | 9 |

| Nationwide | 3.97 | $80 | 6 | 5 |

| Chubb | 3.68 | $109 | 3 | 4 |

| Progressive Commercial | 3.61 | $91 | 8 | 7 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

ERGO NEXT

Best Workers' Comp Insurance in Tennessee

MoneyGeek Rating

4.5/ 5

4.8/5Affordability Score

4.2/5Customer Experience Score

3.5/5Coverage Score

Average Monthly Cost

$62Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

The Hartford

Best Tennessee Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.2/ 5

3.9/5Affordability Score

4.1/5Customer Experience Score

4.3/5Coverage Score

Average Monthly Cost

$81Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

LEARN MORE ABOUT TENNESSEE BUSINESS INSURANCE

Cheapest Workers' Comp Insurance Companies in Tennessee

ERGO NEXT is Tennessee’s cheapest workers’ comp provider at $62 per month ($744 annually). biBERK follows at $72 per month, while Thimble comes in at $74, giving small businesses several affordable options to choose from.

The $47 monthly gap between ERGO NEXT and Chubb, the state’s most expensive provider at $109 per month, adds up to $564 per employee annually. Those savings are most meaningful for businesses with multiple employees in lower-risk industries, where underwriting standards are more consistent across carriers.

| ERGO NEXT | $62 | $744 |

| biBERK | $72 | $864 |

| Thimble | $74 | $888 |

| Hiscox | $78 | $936 |

| Nationwide | $80 | $960 |

| The Hartford | $81 | $972 |

| Simply Business | $81 | $972 |

| Coverdash | $81 | $972 |

| Progressive Commercial | $91 | $1,092 |

| Chubb | $109 | $1,308 |

Cheapest Workers' Comp Insurance in Tennessee by Industry

ERGO NEXT is the cheapest workers’ comp provider in 19 of the 25 industries we analyzed in Tennessee. It's the best starting point for comparison shopping across most business types, with a pricing advantage that's especially noticeable in higher-risk and service-based industries.

The Hartford has the lowest rates in five lower-risk, office-oriented industries, including financial services, consulting, real estate, tech/IT and health care. biBERK leads in just one category, childcare services, at an average of $24 per month. Businesses in that classification can benefit from getting a direct quote rather than defaulting to one of the larger national carriers.

| Financial Services | The Hartford | $9 | $108 |

| Beauty, Body & Wellness Services | ERGO NEXT | $10 | $120 |

| Marketing & Communications | ERGO NEXT | $10 | $120 |

| Consulting Services | The Hartford | $12 | $144 |

| Real Estate & Property Services | The Hartford | $13 | $156 |

| Other Professional Services | ERGO NEXT | $16 | $192 |

| Childcare Services | biBERK | $24 | $288 |

| Food & Beverage | ERGO NEXT | $26 | $312 |

| Tech/IT | The Hartford | $26 | $312 |

| Hospitality, Travel & Tourism | ERGO NEXT | $29 | $348 |

| Healthcare & Medical | The Hartford | $30 | $360 |

| Retail & Product Rental | ERGO NEXT | $34 | $408 |

| Nonprofit & Associations | ERGO NEXT | $38 | $456 |

| Pet Care Services | ERGO NEXT | $38 | $456 |

| Education | ERGO NEXT | $43 | $516 |

| Fitness Services | ERGO NEXT | $43 | $516 |

| Repair & Maintenance | ERGO NEXT | $45 | $540 |

| Arts, Media & Entertainment | ERGO NEXT | $60 | $720 |

| Recreation & Sports | ERGO NEXT | $68 | $816 |

| Cleaning Services | ERGO NEXT | $70 | $840 |

| Manufacturing | ERGO NEXT | $91 | $1,092 |

| Agriculture & Natural Resources | ERGO NEXT | $101 | $1,212 |

| Wholesale & Distribution | ERGO NEXT | $117 | $1,404 |

| Construction & Contracting | ERGO NEXT | $145 | $1,740 |

| Transportation & Logistics | ERGO NEXT | $185 | $2,220 |

How Much Is Workers' Comp Insurance in Tennessee?

Three patterns stood out in our analysis of 25 common industries in Tennessee. First, service and professional industries tend to cluster between $14 and $55 per month per employee. But once physical labor or material handling becomes part of the job, costs rise quickly.

Construction ($224) and transportation ($243) are clear outliers, with average premiums more than double those of the next-highest industries. Statewide averages often understate what higher-risk employers actually pay.

Cleaning services and recreation and sports businesses also pay more than most employers expect. For companies with mixed workforces, accurate employee classification directly affects renewal pricing and overall workers' comp costs.

| Beauty, Body & Wellness Services | $14 | $168 |

| Financial Services | $14 | $168 |

| Marketing & Communications | $14 | $168 |

| Consulting Services | $17 | $204 |

| Real Estate & Property Services | $19 | $228 |

| Other Professional Services | $21 | $252 |

| Childcare Services | $29 | $348 |

| Food & Beverage | $33 | $396 |

| Hospitality, Travel & Tourism | $35 | $420 |

| Tech/IT | $36 | $432 |

| Healthcare & Medical | $41 | $492 |

| Retail & Product Rental | $43 | $516 |

| Nonprofit & Associations | $46 | $552 |

| Pet Care Services | $51 | $612 |

| Fitness Services | $53 | $636 |

| Education | $55 | $660 |

| Repair & Maintenance | $59 | $708 |

| Arts, Media & Entertainment | $75 | $900 |

| Recreation & Sports | $92 | $1,104 |

| Cleaning Services | $95 | $1,140 |

| Manufacturing | $113 | $1,356 |

| Agriculture & Natural Resources | $132 | $1,584 |

| Wholesale & Distribution | $146 | $1,752 |

| Construction & Contracting | $224 | $2,688 |

| Transportation & Logistics | $243 | $2,916 |

Tennessee Workers' Comp Insurance Cost Factors

Tennessee workers' comp rates are filed and approved through the National Council on Compensation Insurance (NCCI), which sets the class code system used by all carriers in the state. The Tennessee Department of Commerce and Insurance oversees market regulation. Tennessee's private competitive structure allows carriers to deviate from NCCI advisory rates, which produces real price variation across providers for the same class code.

How Much Workers' Comp Insurance Do I Need in Tennessee?

Tennessee law requires most employers to carry workers' compensation coverage once you hire five employees, including part-time workers and family members. Construction and coal mining businesses need coverage from day one with your first hire.

The required workers' compensation coverage pays unlimited medical expenses, two-thirds of wages during recovery (capped at $1,426.70 weekly for 2026). Skipping coverage can lead to monetary penalties plus lawsuits from injured workers.

Tennessee Workers' Comp Insurance Exemptions

Most Tennessee employers need workers' comp insurance, but these business categories qualify for exemptions:

- Businesses with fewer than five employees: Employers outside construction and coal mining with four or fewer workers don't need coverage but can purchase it voluntarily.

- Construction service providers on the exemption registry: Sole proprietors, partners, LLC members and corporate officers in construction can register through Tennessee's Secretary of State to exempt themselves while still covering employees.

- Corporate officers (non-construction): Officers file Form I-6 to exempt themselves from coverage. Exempted officers still count toward the employee total unless unpaid.

- Partners and LLC members (non-construction): Business owners are automatically excluded from workers' comp policies but can elect coverage by filing Form I-4.

- State and local government employers: Government entities don't need workers' comp coverage but can provide it for employees.

- Farm labor employers: Businesses employing farm laborers don't need workers' comp coverage under Tennessee law.

- Domestic help employers: Employers hiring domestic workers in private homes don't need workers' comp coverage.

- Independent contractors: Independent contractors aren't considered employees under Tennessee workers' comp law, based on seven factors evaluating the work relationship.

- Casual employees: Workers performing casual employment as defined in Tennessee Code Annotated § 50-6-106 aren't subject to mandatory coverage requirements.

- Self-employed individuals with no employees: Self-employed workers without employees don't need workers' comp. Clients may still request proof of coverage.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal workers' comp programs apply regardless of Tennessee state law for covered employee categories. The Federal Employees' Compensation Act (FECA) covers federal civilian employees. The Federal Employers' Liability Act (FELA) governs railroad workers. The Longshore and Harbor Workers' Compensation Act covers maritime employees. In Tennessee, federal overlap is most relevant for employers near the Port of Memphis and businesses with federal contract workers, who fall under federal jurisdiction rather than Tennessee's Bureau of Workers' Compensation.

How to Get the Best Workers' Comp Insurance in Tennessee

Follow these steps to purchase workers' comp coverage that meets Tennessee's requirements and fits your business profile.

- 1

Confirm Tennessee Coverage Requirements

Check if your business meets Tennessee's employee threshold for mandatory coverage (five or more employees, or one or more for construction and mining). Contact the Tennessee Bureau of Workers' Compensation to confirm your obligations

- 2

Identify Your Class Codes Accurately

The state uses NCCI class codes to assign rates by job type. List every job function performed by your employees and match each to the correct NCCI code. Misclassification can result in audit adjustments at policy year-end. The Tennessee Department of Commerce and Insurance can help you with class code lookup.

- 3

Document Payroll, Employee Count and Claims History

Carriers use payroll figures, employee headcount and prior claims history to calculate your estimated premium and assess risk. Gather at least three years of loss runs from your current insurer before requesting quotes. Accurate payroll documentation reduces the likelihood of large audit adjustments.

- 4

Request Quotes From Multiple Licensed Tennessee Carriers

Tennessee's private competitive market produces real rate variation for the same class code. Pull quotes from at least three to five licensed insurers, including direct carriers and those accessible through licensed brokers. The top-five providers span an $18 per month range from ERGO NEXT at $62 to Nationwide at $80. The full 10-provider dataset shows a $47 per month spread when Chubb at $109 is included.

- 5

Compare Total Value, Not Just Monthly Rate

Premium cost is one factor, but claims handling speed, adjuster responsiveness and policy management tools affect the cost of a workers' comp program. Review each carrier's customer experience scores alongside their rate. A lower monthly rate from a carrier with weak claims support can cost more in the long term.

- 6

Complete Purchase and Establish Payroll and Audit Reporting

After selecting a carrier, complete the application and bind coverage before your required effective date. Set up payroll reporting to track covered wages throughout the policy period. Tennessee workers' comp policies are audited at year-end. Clean payroll records reduce the risk of audit-driven premium adjustments at renewal.

- 7

Review at Annual Renewal

Tennessee workers' comp premiums shift at renewal based on updated payroll, class code changes and your experience modification rate (EMR). Pull your renewal quote at least 60 days before expiration to leave time to re-shop the market if rates have increased. A declining EMR from improved safety performance is the most reliable way to reduce your Tennessee workers' comp premium over time.

Bottom Line

ERGO NEXT has the best workers' compensation insurance for most Tennessee small businesses, combining the state's lowest rate at $62 a month. The Hartford is the better option for employers in higher-risk industries where claims handling depth matters more than entry-level pricing. biBERK offers a reliable middle ground for businesses that want a nationally recognized carrier at a rate close to ERGO NEXT's. The right choice for your business depends on your industry, claims history and how much weight you place on service quality versus premium cost.

Next Steps

Tennessee workers' comp rates vary by industry, employee count and carrier, so the estimates on this page are a starting point rather than a final price. Use the resources below to move from research to purchase.

Tennessee Workers' Compensation Insurance FAQs

What are the penalties for not carrying workers' comp insurance in Tennessee?

Tennessee employers who fail to carry required workers' comp coverage can receive stop-work orders and civil monetary penalties assessed by the Tennessee Bureau of Workers' Compensation. Penalty amounts are subject to annual adjustment.

Does Tennessee workers' comp cover employees who work remotely in other states?

Tennessee workers' comp covers employees whose employment is principally located in Tennessee, even if they occasionally work in other states. Employers with remote workers based permanently in another state should carry coverage in that state as well. Many Tennessee policies include an "other states" endorsement that extends coverage automatically, but confirm the endorsement language with your carrier before relying on it for multi-state exposure.

How does an experience modification rate affect my Tennessee workers' comp premium?

Tennessee uses the NCCI experience modification rate (EMR) to adjust premiums based on a business's actual claims history relative to expected losses for its industry. An EMR below 1.0 reduces your premium; an EMR above 1.0 increases it. Businesses with three or more years of payroll history and sufficient premium volume are eligible for experience rating. Reducing workplace injuries is the most direct way to lower your EMR over time.

Can business owners opt out of workers' comp coverage in Tennessee?

Corporate officers and LLC members in Tennessee may elect to exclude themselves from workers' comp coverage by filing the appropriate exclusion form with their insurer, subject to limits set by Tennessee law. Sole proprietors without employees are not required to carry coverage but may purchase it voluntarily. Partners in a partnership may also opt out for themselves while maintaining coverage for their employees. Verify current exclusion procedures with the Tennessee Bureau of Workers' Compensation.

What is the difference between workers' comp and employer's liability insurance in Tennessee?

Workers' comp covers medical expenses and lost wages for employees injured on the job, regardless of fault. Employer's liability, included as Part Two of most workers' comp policies, covers the employer against lawsuits from employees who allege negligence beyond what workers' comp provides. In Tennessee, employer's liability applies in cases involving third-party-over actions or when an injured worker's family member brings a related claim.

How long does a workers' comp claim stay on my Tennessee premium record?

Workers' comp claims affect your Tennessee premium for three policy years through the experience modification rate calculation. The EMR uses a rolling three-year window of loss data, excluding the most recent completed policy year. A single large claim can elevate your EMR for multiple renewal cycles. Loss control and early return-to-work programs are cost-effective investments for Tennessee employers with any frequency of workplace injuries.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Tennessee using small business profiles with one to four employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate a MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.

Sources

- National Council on Compensation Insurance. "ABCs of Experience Rating." Accessed July 8, 2026.

- National Council on Compensation Insurance. "Frequency and Severity Results by State Based on Data Valued as of December 31, 2023." Accessed July 8, 2026.

- National Federation of Independent Business. "TN Workers' Comp Rates to Decline for 11th Year in a Row." Accessed July 8, 2026.

- Tennessee Bureau of Workers' Compensation. "New Program Aims to Help Employees, Reduce Workers' Compensation Costs." Accessed July 8, 2026.

- Tennessee Bureau of Workers' Compensation. "REWARD Toolkit." Accessed July 8, 2026.

- Tennessee Department of Labor and Workforce Development. "How Rates for Insurance Premiums are Set." Accessed July 8, 2026.

- Tennessee Department of Labor and Workforce Development. "Who Must Carry Insurance." Accessed July 8, 2026.