ERGO NEXT has the best Oklahoma workers' comp insurance, combining the state's lowest monthly rate with top customer experience scores. The Hartford and biBerk are strong alternatives, each offering competitive pricing and broad industry eligibility.

Best Workers' Comp Insurance in Oklahoma (2026)

With rates starting at $9 monthly, ERGO NEXT, The Hartford and biBerk offer the cheapest and best workers' comp insurance in Oklahoma.

Get matched to top Oklahoma workers' comp insurance providers and find your ideal coverage.

Select state

Updated: June 27, 2026

Advertising & Editorial Disclosure

ERGO NEXT offers the top cheap workers' compensation insurance in Oklahoma. The following are the state's cheapest and best workers' comp insurance providers and their average monthly rates:

- ERGO NEXT: $77 a month

- Thimble: $80 a month

- biBerk: $83 a month

- The Hartford: $86 a month

- Coverdash: $94 a month

Oklahoma requires most employers with one or more employees to carry workers' comp insurance, though sole proprietors and certain corporate officers may opt out of coverage. Employers who fail to carry required coverage face penalties including fines and potential civil liability. Some business owners choose to opt in voluntarily even when exempt to protect themselves from out-of-pocket medical and wage costs.

The average cost of workers' comp insurance in Oklahoma cost is $94 monthly per employee, but rates vary widely by industry. The cheapest industry in the state is Beauty, Body & Wellness Services at $15 a month, while Transportation & Logistics is the most expensive at $287 a month.

Oklahoma operates as a private competitive market with no state fund, meaning employers can get workers' comp coverage directly from licensed private insurers. If your business is declined by standard carriers, Oklahoma's assigned risk pool provides fallback coverage as a market of last resort. Comparing quotes from multiple carriers is the most reliable way to find competitive pricing.

Oklahoma workers' comp insurance covers the following:

- Medical expenses for work-related injuries and illnesses

- Wage loss benefits capped at 70% of the employee's average weekly wage, not to exceed the state's average weekly wage

- Vocational rehabilitation services to support return to work

- Death benefits and burial expenses for dependents of workers killed on the job

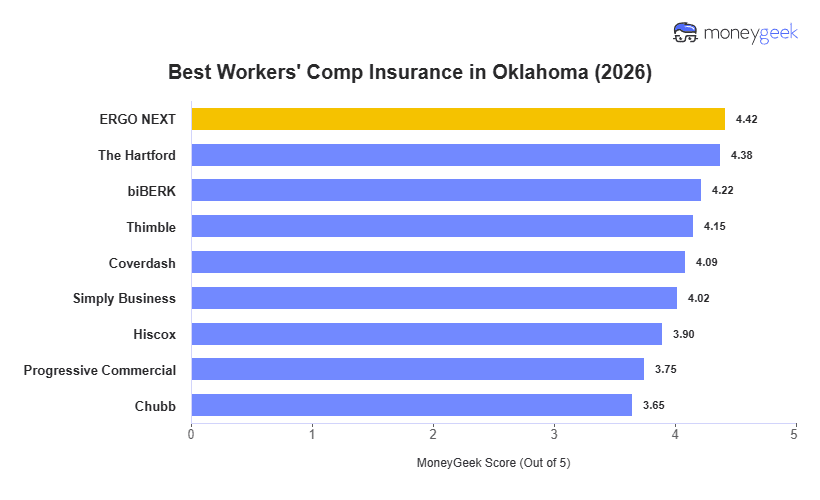

Best Workers' Comp Insurance Companies in Oklahoma

| ERGO NEXT | 4.42 | $77 | 1 | 5 |

| The Hartford | 4.38 | $86 | 3 | 3 |

| biBERK | 4.22 | $83 | 7 | 7 |

| Thimble | 4.15 | $80 | 7 | 8 |

| Coverdash | 4.09 | $94 | 5 | 1 |

| Simply Business | 4.02 | $98 | 2 | 2 |

| Hiscox | 3.90 | $97 | 6 | 9 |

| Progressive Commercial | 3.75 | $99 | 7 | 6 |

| Chubb | 3.65 | $131 | 3 | 4 |

How Did We Determine These Rates and Rankings?

These rates are estimates based on MoneyGeek's analysis of small businesses with one to four employees across 408 major industries. Actual rates vary based on your business location, industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

ERGO NEXT

Best Workers' Comp Insurance in Oklahoma

MoneyGeek Rating

4.4/ 5

4.8/5Affordability Score

4.2/5Customer Experience Score

3.5/5Coverage Score

Average Monthly Cost

$77Claims Processing Score

4/5Policy Management Score

4.1/5Buying Process Score

4.4/5

The Hartford

Best Oklahoma Workers' Comp Insurance: Runner-Up

MoneyGeek Rating

4.4/ 5

4.4/5Affordability Score

4.3/5Customer Experience Score

4/5Coverage Score

Average Monthly Cost

$86Claims Processing Score

4.1/5Policy Management Score

4/5Buying Process Score

4/5

LEARN MORE ABOUT OKLAHOMA BUSINESS INSURANCE

Cheapest Workers' Comp Insurance Companies in Oklahoma

ERGO NEXT is Oklahoma’s cheapest workers’ comp provider at $77 per month ($924 annually), about 18% below the state average of $94. Thimble follows at $80 monthly, with biBerk at $83, giving small businesses three workers’ comp options under $85 per month in Oklahoma’s competitive private market.

The pricing gap between ERGO NEXT ($77 a month) and Chubb ($131 a month) amounts to $648 per employee annually. These savings are most meaningful for businesses with multiple employees and clean claims histories, but the pricing gap shrinks in high-risk industries, where underwriting factors reduce differences between carriers.

| ERGO NEXT | $77 | $924 |

| Thimble | $80 | $960 |

| biBERK | $83 | $996 |

| The Hartford | $86 | $1,032 |

| Coverdash | $94 | $1,128 |

| Hiscox | $97 | $1,164 |

| Simply Business | $98 | $1,176 |

| Progressive Commercial | $99 | $1,188 |

| Chubb | $131 | $1,572 |

Cheapest Workers' Comp in Oklahoma by Industry

The Hartford is the cheapest workers' comp provider in more Oklahoma industries than any other carrier in our analysis. With the lowest rates in 12 of the 25 industries we reviewed, its wins are concentrated in office-based and professional work, where monthly rates start at $9 for financial services and top out at $106 for manufacturing.

ERGO NEXT is the cheapest for most high-risk industry in our analysis, posting the lowest rates for Construction, Transportation & Logistics, Agriculture, Cleaning Services, and Recreation & Sports. If your business involves physical labor or fleet vehicles, ERGO NEXT belongs at the top of your comparison list.

| Financial Services | The Hartford | $9 | $108 |

| Beauty, Body & Wellness Services | The Hartford | $11 | $132 |

| Marketing & Communications | The Hartford | $12 | $144 |

| Consulting Services | The Hartford | $13 | $156 |

| Real Estate & Property Services | The Hartford | $14 | $168 |

| Other Professional Services | The Hartford | $17 | $204 |

| Childcare Services | biBERK | $27 | $324 |

| Tech/IT | The Hartford | $27 | $324 |

| Hospitality, Travel & Tourism | The Hartford | $30 | $360 |

| Food & Beverage | ERGO NEXT | $32 | $384 |

| Healthcare & Medical | The Hartford | $32 | $384 |

| Retail & Product Rental | The Hartford | $37 | $444 |

| Nonprofit & Associations | The Hartford | $42 | $504 |

| Pet Care Services | biBERK | $47 | $564 |

| Fitness Services | biBERK | $51 | $612 |

| Education | Thimble | $54 | $648 |

| Repair & Maintenance | ERGO NEXT | $58 | $696 |

| Arts, Media & Entertainment | biBERK | $74 | $888 |

| Recreation & Sports | ERGO NEXT | $86 | $1,032 |

| Cleaning Services | ERGO NEXT | $87 | $1,044 |

| Manufacturing | The Hartford | $106 | $1,272 |

| Agriculture & Natural Resources | ERGO NEXT | $126 | $1,512 |

| Wholesale & Distribution | biBERK | $147 | $1,764 |

| Construction & Contracting | ERGO NEXT | $183 | $2,196 |

| Transportation & Logistics | ERGO NEXT | $232 | $2,784 |

How Much Is Workers' Comp Insurance in Oklahoma?

Oklahoma's average workers' comp cost is $94 monthly per employee, above the national average of $74 a month. The cheapest industry is Beauty, Body and Wellness Services at $15 a month, while Transportation and Logistics is the most expensive at $287 a month.

The steepest jump in our analysis lies in the midrang tier. Industries like Cleaning Services ($112 a month) and Manufacturing ($133 a month) pay more than double what Retail ($51) pays, despite all three involving physical labor. That gap reflects Oklahoma's classification system. Cleaning and manufacturing workers file claims at higher rates and with greater severity than general retail workers, which pushes those premiums up sharply.

| Beauty, Body & Wellness Services | $15 | $180 |

| Financial Services | $15 | $180 |

| Marketing & Communications | $15 | $180 |

| Consulting Services | $20 | $240 |

| Real Estate & Property Services | $21 | $252 |

| Other Professional Services | $23 | $276 |

| Childcare Services | $34 | $408 |

| Food & Beverage | $38 | $456 |

| Hospitality, Travel & Tourism | $40 | $480 |

| Tech/IT | $41 | $492 |

| Healthcare & Medical | $47 | $564 |

| Retail & Product Rental | $51 | $612 |

| Nonprofit & Associations | $54 | $648 |

| Pet Care Services | $59 | $708 |

| Fitness Services | $62 | $744 |

| Education | $63 | $756 |

| Repair & Maintenance | $69 | $828 |

| Arts, Media & Entertainment | $87 | $1,044 |

| Recreation & Sports | $108 | $1,296 |

| Cleaning Services | $112 | $1,344 |

| Manufacturing | $133 | $1,596 |

| Agriculture & Natural Resources | $155 | $1,860 |

| Wholesale & Distribution | $171 | $2,052 |

| Construction & Contracting | $262 | $3,144 |

| Transportation & Logistics | $287 | $3,444 |

Oklahoma Workers' Comp Insurance Cost Factors

Oklahoma workers' comp rates are filed with the National Council on Compensation Insurance (NCCI) and regulated by the Oklahoma Insurance Department. The state operates as a private competitive market, meaning carriers set their own rates within NCCI's approved loss cost framework. Oklahoma's high share of high-hazard industries is the single most distinguishing cost driver in the state.

How Much Workers' Comp Insurance Do I Need in Oklahoma?

Oklahoma law mandates workers' compensation insurance for nearly all employers, regardless of employee count. Your coverage amounts depend on total payroll and industry classification, not fixed dollar limits. Policies must provide unlimited medical benefits and wage replacement at 70% of average weekly wages, up to $1,128.66 weekly for 2026 injuries. Failing to maintain required workers' compensation coverage can result in misdemeanor charges, fines and potential business closure.

Oklahoma Workers' Comp Insurance Exemptions

While you're often required to have coverage in Oklahoma, some business categories are exempt from workers' comp requirements:

- Sole Proprietors: Sole proprietors with no employees are not required to carry workers' comp coverage, but may elect to cover themselves voluntarily to protect against personal income loss from a work-related injury.

- Corporate Officers: Officers of corporations may elect to exclude themselves from coverage by filing the appropriate form with their insurer. Verify current opt-out procedures with the Oklahoma Workers' Compensation Commission.

- Partners: Partners in a general partnership are generally exempt from mandatory coverage requirements but may opt in voluntarily.

- Independent Contractors: Properly classified independent contractors are not employees and are not covered under an employer's workers' comp policy. Misclassification exposes employers to substantial liability.

- Domestic Workers: Workers employed in private households, such as housekeepers or nannies, are generally exempt from Oklahoma's mandatory workers' comp requirements.

- Agricultural Workers: Agricultural laborers employed by farm operators meeting specific size thresholds may be exempt. Verify current thresholds with the Oklahoma Workers' Compensation Commission.

- Casual Workers: Workers hired for occasional, incidental tasks not in the course of the employer's regular business may qualify for the casual worker exemption under Oklahoma law.

FEDERAL WORKERS' COMP PROGRAMS OVERRIDE STATE REQUIREMENTS

Federal workers' comp programs apply to specific employee categories regardless of Oklahoma state law. The Federal Employees' Compensation Act (FECA) covers federal civilian employees. The Federal Employers' Liability Act (FELA) governs railroad workers. The Longshore and Harbor Workers' Compensation Act covers maritime employees working on navigable waters. In Oklahoma, federal installations and interstate railroad operations fall under these federal frameworks, and employers in those sectors must comply with federal requirements rather than, or in addition to, the Oklahoma Workers' Compensation Commission's rules.

How to Get the Best Workers' Comp Insurance in Oklahoma

Getting workers' comp insurance in Oklahoma requires confirming your legal obligations, classifying your workforce accurately, and comparing licensed carriers. Follow these steps to secure the right coverage for your business. See our full guide on how to get workers' compensation insurance for additional detail.

- 1

Confirm Oklahoma Coverage Requirements

Verify whether your business meets the employee threshold that triggers mandatory coverage under Oklahoma law. Contact the Oklahoma Workers' Compensation Commission to confirm your obligations, including any exemptions that apply to your ownership structure or workforce type. Document your determination before requesting quotes.

- 2

Identify Your Class Codes Accurately

NCCI class codes define the occupational risk category for each employee and directly determine your base premium. Review the job duties of every employee and match them to the correct NCCI class code. You can do this by using the Oklahoma Insurance Department's resources or a licensed agent. Incorrect class code assignments result in audit adjustments and potential coverage gaps.

- 3

Document Payroll, Employee Count, and Claims History

Collect your total annual payroll by class code, your current employee count and a three-to-five year loss run from any prior workers' comp carrier. Carriers use this information to calculate your experience modification rate (EMR) and assess underwriting risk. Clean documentation speeds up the process.

- 4

Request Quotes From Multiple Licensed Oklahoma Carriers

Pull quotes from at least three carriers licensed to write workers' comp in Oklahoma, including direct writers like ERGO NEXT and The Hartford as well as independent agents who can access multiple markets. Oklahoma pricing varies by $17 or more per employee per month across the five featured carriers, which makes comparing quotes essential before committing.

- 5

Compare Total Value, Not Just Monthly Rate

Look at each quote for claims processing capability, policy management tools, audit procedures and financial strength in addition to the monthly premium. A carrier with a lower rate but slower claims handling may cost more in lost productivity and employee relations over time. Review each carrier's CX scores and coverage rank.

- 6

Complete Purchase and Establish Payroll and Audit Reporting

Complete the application, bind coverage and set up your payroll reporting schedule. Oklahoma workers' comp policies are typically audited at renewal based on actual payroll. Establish accurate payroll records from day one to avoid large audit adjustments at the end of the policy term.

- 7

Review at Annual Renewal

Before each annual renewal, audit your class codes, employee count and payroll estimates for accuracy. Changes in business operations, new hires or shifts in job duties can require class code updates. Pull competing quotes at renewal to confirm your current provider remains competitive in Oklahoma's market.

Bottom Line and Next Steps

ERGO NEXT is the best workers' comp provider for most Oklahoma small businesses. The Hartford is the better option for employers in high-hazard industries who prioritize claims support, while biBerk offers a competitive middle-ground for businesses seeking a nationally recognized carrier below $85 a month. The right choice balances your industry risk profile, employee count and tolerance for claims process complexity.

Next Steps

Oklahoma workers' comp rates vary by industry, carrier, and individual business risk profile. Use the resources below to move from comparison to coverage.

Oklahoma Workers' Compensation Insurance FAQs

Carrying workers' comp coverage prevents non-compliance penalties but doesn't eliminate all liability exposure. Oklahoma employers without required coverage face civil fines, stop-work orders and personal liability for employee injury costs. Confirm current penalty amounts with the Oklahoma Workers' Compensation Commission, since fine structures are subject to legislative revision.

Oklahoma workers' comp policies generally cover employees whose employment is principally located in Oklahoma, even when they temporarily work in another state. If an employee permanently relocates to another state, that state's coverage requirements may apply. Notify your carrier of any employees who work across state lines to confirm your policy includes the appropriate other-states coverage endorsement.

An EMR above 1.0 increases your premium, while an EMR below 1.0 reduces it. Oklahoma uses NCCI's experience rating formula. This compares your actual losses to expected losses for your industry and size. A single large claim can increase your EMR for up to three policy years, making proactive safety programs and prompt claims reporting important cost controls.

Sole proprietors and certain corporate officers in Oklahoma may choose to exclude themselves from coverage by filing the appropriate exclusion form with their insurer. Partners in general partnerships are exempt by default. Opting out means the owner assumes personal financial responsibility for any work-related injury costs. Confirm current opt-out procedures and eligibility criteria with the Oklahoma Workers' Compensation Commission before making this election.

Workers' comp covers an employee's medical expenses and lost wages after a work-related injury without requiring proof of employer fault. Employer's liability insurance, included as Part Two of a workers' comp policy, covers the employer if an injured worker sues for damages beyond the workers' comp benefit schedule. In Oklahoma, both coverages are in a standard workers' comp policy.

Workers' comp claims affect an Oklahoma employer's experience modification rate for approximately three policy years under NCCI's experience rating formula. The most recent policy year is excluded from the EMR calculation. This means that a claim filed this year will influence premiums for the following three renewal cycles. Closing claims quickly and implementing return-to-work programs can limit the long-term premium impact.

MoneyGeek analyzed workers' comp insurance rates and provider performance across Oklahoma using small business profiles with one to four employees spanning 408 major industries. Companies earn up to five points in each category in our scoring system. We then use a weighted average of these category scores to calculate an overall MoneyGeek score out of five.

- Affordability (55%): Based on average payroll for the most common employee code per industry and state classification, priced per employee for a one to four employee business.

- Customer Experience (35%): Evaluates buying (20%), which covers quote access, pricing accuracy and sales support; policy management (30%), which covers payroll reporting, audits, billing and loss control; and claims (50%), which covers FNOL speed, adjuster support, medical access, wage replacement and dispute handling.

- Coverage Options (10%): Assesses coverage completeness (35%), including employers' liability and wage and medical reimbursement; policy flexibility and endorsements (25%); eligibility, state and industry breadth (20%); and policy terms, limits and exclusions (20%).

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work have been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes content for real pet owners.

Questions about MoneyGeek's business or pet insurance content? Reach him at connor@moneygeek.com or on LinkedIn.

Sources

- Insurance Journal. "Oklahoma Governor Signs Workers' Compensation Overhaul." Accessed August 10, 2026.

- Insurance Journal. "Oklahoma Lawmakers Pass Workers' Comp Reform Legislation." Accessed August 10, 2026.

- National Council on Compensation Insurance. "ABCs of Experience Rating." Accessed August 10, 2026.

- Oklahoma Insurance Department. "Insurance Commissioner Approves Loss-Cost Reduction for 2025 Workers' Compensation." Accessed August 10, 2026.

- Oklahoma Workers' Compensation Court of Existing Claims. "Employer's FAQ." Accessed August 10, 2026.