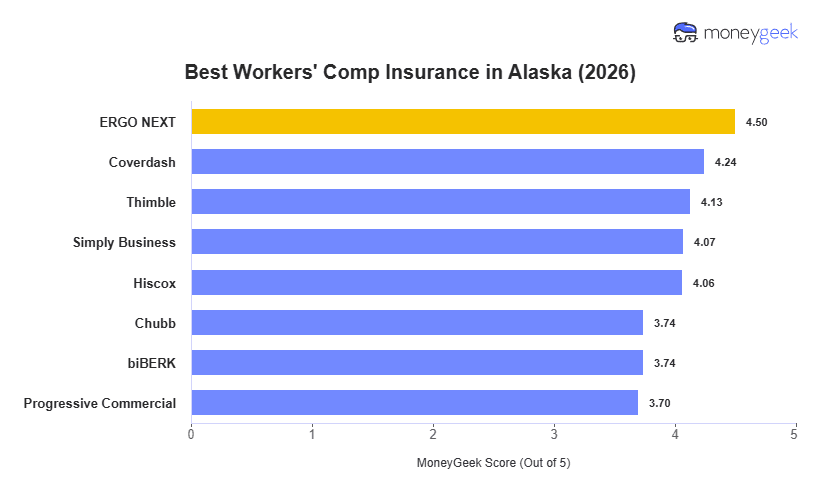

ERGO NEXT is the best workers' comp insurance provider in Alaska with the lowest average rates and the top buying experience among providers we reviewed. Coverdash follows in second place, offering the state's best coverage score. Both are strong options for Alaska employers shopping for workers' comp insurance.

The spread between ERGO NEXT ($132 a month) and the most expensive provider (Chubb at $231 a month) is $99. Low-hazard Alaska employers gain the most from that gap. The advantage narrows for construction and transportation class codes where all carriers converge on higher base rates.