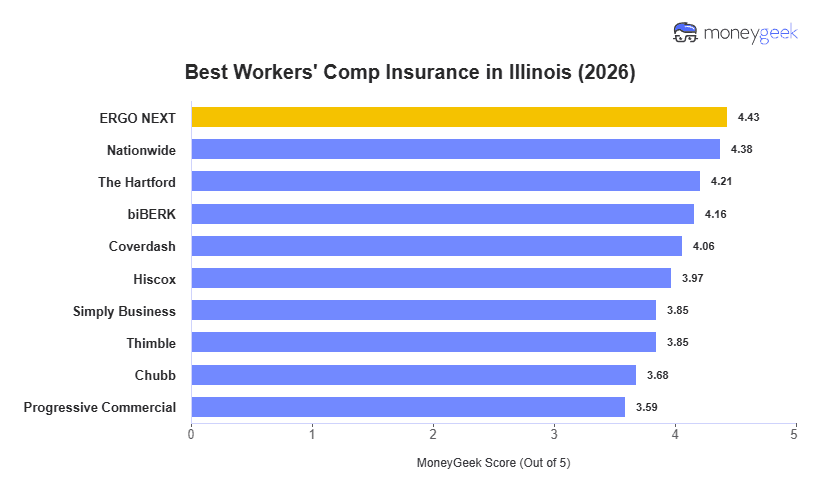

ERGO NEXT is the best workers' comp insurance provider in Illinois overall at $110 monthly, leading the group in customer service. Illinois small businesses can get workers' compensation insurance for an average of $109 per month through Nationwide, the lowest-cost option in MoneyGeek's analysis of 10 providers. The Hartford rounds out the top three at $141 per month, ranking third in both coverage and customer service.

Rates across all 10 providers range from $109 to $190 monthly, based on MoneyGeek's analysis of small businesses with one to four employees. Your actual rate will vary based on your industry, claims history and coverage limits.